Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Seabrook, WA: Your Next Great Escape

Summer has arrived, and if you are looking for a great escape only 3 hours from Seattle, you should check out Seabrook on the Washington Coast! I had the opportunity to enjoy it this winter, and I am excited to share all the aspects this gem of a town has to offer, along with a discount you can use for your stay. This town can be enjoyed through all four seasons, but summer has to be amazing!

I can extend to you a 20% discount off your stay. Seabrook and Windermere  have partnered, and Windermere has become the official real estate company representing Seabrook. This partnership allows us to pass on this discount to our clients who would like to visit. If you are interested in receiving the discount, please reach out, and I can get you registered and personally connect you with the Seabrook rental team to ensure you get to enjoy this special offer.

have partnered, and Windermere has become the official real estate company representing Seabrook. This partnership allows us to pass on this discount to our clients who would like to visit. If you are interested in receiving the discount, please reach out, and I can get you registered and personally connect you with the Seabrook rental team to ensure you get to enjoy this special offer.

Seabrook is a beach town along the Washington Coast’s Olympic Peninsula that is seamlessly woven into nature. The town sits on a scenic bluff overlooking the Pacific Ocean, offering incredible views and unmatched beach access. Seabrook is a thoughtfully-built new town founded on new urbanism design.

Seabrook features over 475+ Washington Coast homes in eight neighborhoods, some available as vacation rentals and some available for purchase, as well as numerous merchants, more than 30 parks, a Town Hall, and countless amenities. Seabrook is a walking and biking paradise! Designed with a “walk to anything in five minutes” principle in mind, guests and residents routinely comment on the thoughtful design their team has employed to create this unique vacation town.

Every year, thousands of guests stay at Seabrook by booking one of the over 270 homes in their popular Vacation Rentals program. No home is the same, accommodating anywhere from two to twenty people (dogs, too, in certain homes).

In addition to promenades and walking trails galore, you’ll find a central amphitheater, a hilltop and oceanfront park, outdoor games and playgrounds, a Town Hall, fire pits, horseshoe pits, mountain bike trails, a heated indoor pool, and spacious Crescent Park. Leave the car in park and explore simple living on the Washington Coast.

All of the homes come with well-appointed kitchens, but we all know that grabbing a bite to eat while on vacation is a bonus. Whether you’re looking for a romantic dinner, a family-friendly meal, or coffee before a beach walk, Seabrook offers dining options for every taste, all within an easy stroll of the town center.

- Frontager’s Pizza Co. – Wood-fired pizza, pasta, salads, local beer & wine.

- Koko’s Restaurant & Tequila Bar – Elevated Mexican cuisine, craft margaritas, weekend brunch.

- Rising Tide Tavern – Burgers, seafood, fish & chips, salads, and local brews.

- The Stowaway Wine Bar – Wine, charcuterie, and small plates in a cozy setting.

- Vista Bakeshop – Fresh pastries, breakfast sandwiches, artisan breads, and coffee.

- Bellwether Cafe – Espresso drinks, breakfast, sandwiches, and grab-and-go options.

- The Sweet Life – Ice cream, candy, fudge, and milkshakes.

SEABROOK AND THE ART OF TOWNMAKING

Town founders, Casey and Laura Roloff, first met in high school and quickly realized they had one major thing in common — they loved the beach! After graduating from college, they married and moved to the Oregon Coast, where they started their very first business painting houses.

As the Roloffs became more involved in the local community, they studied the local and national real estate markets and recognized an opportunity to build custom vacation homes, second homes, and primary residences that had architectural character and an uncommon attention to detail.

Using new urbanist design principles and inspiration from the internationally recognized town of Seaside, Florida, they set out to build their first beach community, Bella Beach, on the Oregon Coast. Finding great success with Bella, they eventually looked northward towards Washington State for a similar opportunity. This led them to Grays Harbor County, where, in 2004, along with their innovative design team, they worked collaboratively to curate and develop Washington’s most celebrated beach town, Seabrook.

A TOWN WITH A PEDESTRIAN-FRIENDLY SCALE

Visitors to Seabrook experience how the lost art of town making has been brought to life with a specialized design concept known as The New Urbanism. Everything in the coastal town is purpose-built with walkability and connectivity intertwined with the beautiful coastal surroundings, a signature of the Pacific Northwest.

Entering Seabrook is stepping into a welcoming, comfortable and charming atmosphere that has all been carefully planned and accomplished one home, retail space, amenity, or trail at a time. Yes, cars are welcome (how else are you going to get there?), but you’ll be happy to leave them stowed away in a carriage house or along one of the tree-lined streets where on-street parking is actually encouraged to ensure safe streets for pedestrians and bicyclists.

INTENTIONAL EASE OF ACCESS

The transect concept provides zones that are an important part of new urbanism planning and that help describe the wide range of community transitions from rural to urban with an emphasis of increasing town-wide accessibility to homes, shopping, and amenities.

Proximity To Metropolitan Areas

Seabrook is conveniently located a short drive away from Seattle and Portland, making it an accessible drive-to vacation location that has been on-the-rise for years. The beach town is also situated near popular sightseeing destinations like the Olympic National Park (a World Heritage Site), a 45-minute drive away.

Homes to Accommodate Everyone

Seabrook was built with inclusivity in mind. Homes of all sizes, from 2-person carriage homes to homes that sleep upwards of 20 people, create a sense of community for everyone living or staying in Seabrook.

Merchants & Town Events

In Seabrook, children play freely and safely, merchants quickly become staple stops of old and new patrons alike, and events bring the community together for conversation and memories made. They even have venues you can rent for your own special events such as a wedding.

Miles of Shoreline and Trails to Explore

But we can’t forget about the beach. All roads (or, in Seabrook’s case, walking trails) flow down to the magnificent allure of the Pacific Ocean. Seabrook’s three beach accesses provide a convenient way to enjoy and access the beach from its three oceanfront neighborhoods: NW Glen, Pacific Glen, & Elk Creek.

Community Involvement

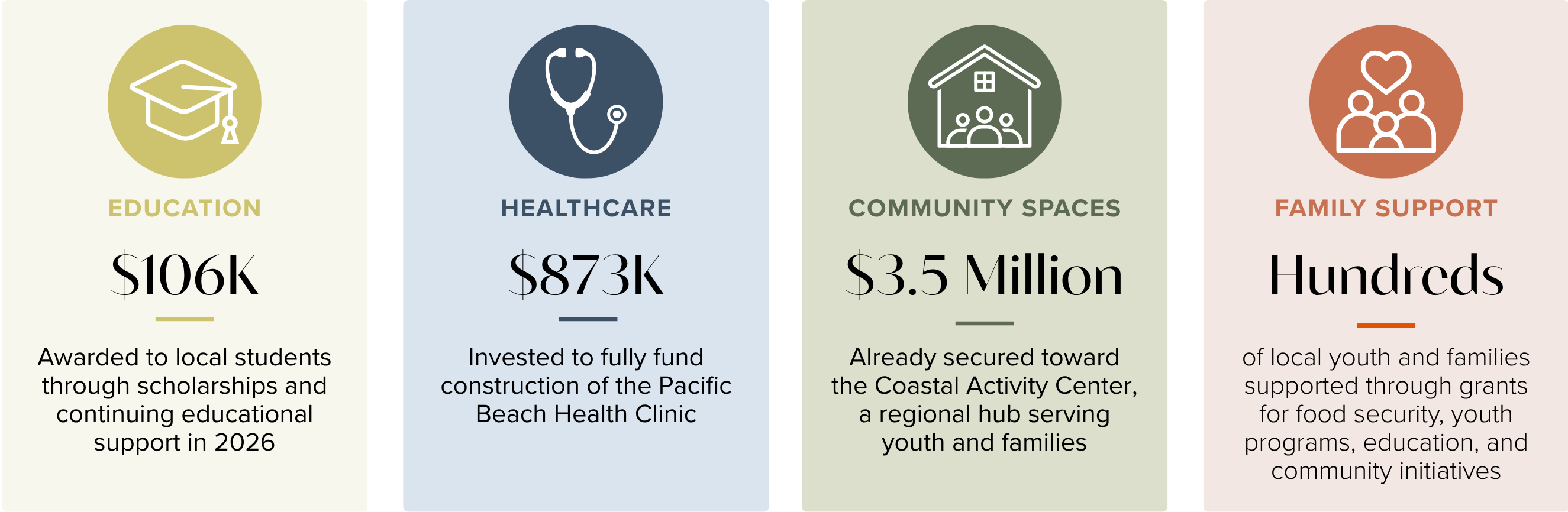

The connectivity also expands throughout the local community and county. The Seabrook Community Foundation awards grants to many Grays Harbor County Nonprofits with an emphasis on aiding Grays Harbor Youth. One percent of every house sale goes towards the efforts to uplift the North Beach community that surrounds Seabrook.

I highly encourage you if you have a blank space in your calendar this summer or any other time of the year to visit Seabrook. Its charm, connection to nature, and easy access from the city makes it a great place to invest your vacation dollars. If you are interested in exploring the real estate market there, please reach out. I have connections to the sales team now that they are a Windermere affiliate. Here’s to a beautiful summer ahead and finding some time to wind down with the people that matter most.

Design Trends for 2026 & Beyond: Softer, Lived-In Luxury

As we find ourselves in the midst of spring, freshening up our surroundings is a natural inclination. If you have been dreaming of updating your space, trying something new, or just want an overall refresh, I’ve uncovered the latest trends to help inspire your next project. Don’t miss all the fun links below that help bring these trends to life.

As a broker who is in and out of hundreds of homes a year, I can definitely say these simple pivots can add enjoyment plus resale value to your home. Many of these design trends can be done on your own or involve minor changes that make a big impact without breaking the bank. Some are more involved, but if you are considering a remodel, these great tips will help ensure your investment is on track.

The biggest home design trends for 2026 are all about warmth, texture, personality, and nature-inspired living. After years of ultra-minimal, gray-and-white interiors, designers are moving toward homes that feel layered, emotional, and timeless rather than overly “perfect.”

Here’s a breakdown of the top trends across paint, decor, surfaces, kitchens, baths, and landscaping.

- Paint Color Trends for 2026

Warm Earthy Neutrals Replace Cool Gray

Designers are calling these “grounding neutrals. The dominant palette for 2026 is:

- warm taupe

- mushroom

- khaki

- camel

- espresso brown

- clay and terracotta

- olive and eucalyptus greens

Most talked-about tones:

- Sherwin-Williams “Universal Khaki”

- Benjamin Moore “Silhouette” (deep espresso-charcoal)

- Valspar “Warm Eucalyptus”

- rich browns and muddy greens

Best Seattle-Friendly Paint Colors

These work especially well in cloudy PNW lighting:

- Benjamin Moore Swiss Coffee

- Benjamin Moore White Dove

- Benjamin Moore Pale Oak

- Benjamin Moore Edgecomb Gray

- Sherwin-Williams Alabaster

- Sherwin-Williams Accessible Beige

- Sherwin-Williams Drift of Mist

- Sherwin-Williams Greek Villa

- Sherwin-Williams Shoji White

Color Drenching Continues

Color drenching, which involves rooms painted in a single tone, including walls, ceilings, trim, and cabinetry, is still trending strongly in 2026. This creates a cocoon-like, luxurious feel. Popular drenched colors:

Soft Pastels Are Back, But Sophisticated

Soft pastels are being used in a more grown-up, vintage-inspired way rather than in a playful or childish way. Popular colors that add warmth and softness are:

- Interior Decor Trends

“Lived-In Luxury”

Lived-in Luxury is a design style that makes a home feel elevated, beautiful, and curated, but also comfortable, warm, personal, and actually livable. The aesthetic is cozy sophistication instead of sterile minimalism. Homes are becoming:

- softer

- more personal

- less staged

- more collected over time

Expect:

- antiques mixed with modern

- handmade pottery

- layered textiles

- books everywhere

- artisan lighting

- vintage rugs

Curves & Organic Shapes

Sharp modern edges are softening. The aesthetic in 2026 includes:

Statement Lighting as Art

Lighting is now treated like jewelry for the room rather than a utility. I’ve been impressed with lighting options that are not overly expensive, and the impact that is made is huge. Simply replacing a “boob” light in a bedroom with something more elevated or a bar light above a bathroom mirror that has more appeal can change the feel of the entire room and elevate it. Lighting is becoming sculptural:

Chrome Is Back

Warm brass still exists, but polished chrome and nickel are returning in a cleaner, more timeless way. I am also seeing a trend of mixed metals rise to the top. Along with the layered, more collected look, having a balanced variety instead of just one tone throughout creates a cozier, more interesting space.

Especially trending in:

- kitchens

- baths

- cabinet hardware

- faucets

Wallpaper is no longer just “pattern.”

Wallpaper is having a MASSIVE moment in 2026, but it looks very different from the wallpaper trends people remember from the 1990s or even the accent-wall era of the 2010s. The biggest shift is that it’s becoming immersive, tactile, and soulful. Expect:

- texture

- atmosphere

- architecture

- storytelling

- emotional design

- Hard Surface Trends

Natural Stone with Movement

While new paint, switching out hardware, and updating lighting can be somewhat easy and less costly, new hard surfaces are a bigger investment. If you are considering replacing your countertops, choosing dramatic natural stone instead of plain quartz is the direction we are seeing designers go. The more movement and organic texture, the better. Even a quartz with some veins has been popular versus something more plain.

Trending:

Warm Woods Dominate

White oak remains huge, but darker woods are rising:

- walnut

- smoked oak

- medium brown woods

- rich paneling

Warm wood paneling is especially trending in mid-century modern homes and recently-built modern new construction homes. Gone are the days when wood paneling is frowned upon. I’m even seeing older homes that still have original wood paneling be preserved and highlighted. There are really fun wood paneling kits that are available to do an accent wall, stairwell, or end of a hallway to add depth, texture, and warmth.

Textured Finishes

Flat, sterile finishes are fading, and imperfection is now considered luxurious. This aligns with the more curated, collected feel that lends itself to coziness and evokes emotion.

Trending textures:

- limewash walls

- Venetian plaster

- fluted wood

- Zellige tile

- handmade ceramic tile

- textured stone

Tile Trends

Personalized tilework is becoming a major design feature. Tiles with texture, warmth, and variation can make a room feel softer and less stark. Zellige tile, which is intentionally irregular (has differing tile height and imperfect edges), glossy, and reflects light, can be found in whites and creams or in tonal shades, which are big in 2026:

- checkerboard stone

- mosaic tile

- slab backsplashes

- handmade-look tile

- full-height stone walls

- Kitchen Trends

“Soft Kitchens”

Kitchens are becoming warmer and less clinical. Completely white modern kitchens are being replaced with warmer, layered kitchens. Creams and wood are highlights to create dimension, character, and warmth.

Trending:

- wood cabinetry

- creamy paint colors

- hidden appliances

- furniture-style islands

- mixed materials

Mixed Cabinet Colors

Instead of one uniform kitchen look, updates are added to create a very custom-looking space with mixed cabinet colors. As I mentioned above, a mix of hardware and paint can help bring a space to life and add character and charm. This should be done in a well-balanced way to provide a consistent, curated feel.

Integrated Wellness Features

The home is becoming more wellness-centered. Creating spaces to slow down, simplify, and center in health are increasingly popular. Favorite wellness features for kitchens include:

- beverage stations

- hidden pantries

- indoor herb gardens

- filtered water systems

- calming breakfast nooks

- Bathroom Trends

Spa-Like Natural Bathrooms

Bathrooms are becoming retreat spaces and feel more spa-like versus utilitarian. Huge movement toward softening the space by using:

- warm stone

- soft lighting

- plaster finishes

- natural wood vanities

- wet rooms

- freestanding tubs

Statement Stone Slabs

Large slab walls and dramatic stone vanities are replacing busy tile patterns.

Especially popular:

- travertine

- marble-look quartzite

- green-veined stone

- Exterior & Landscaping Trends

Nature-Inspired Exteriors

Exterior palettes are becoming softer, earthier, and more architectural. This is probably the question I am most often asked, “what color should I paint my house?”. Darker exterior colors have been on the rise for some time, and they continue to stay there, but with a bend towards earth tones such as sage green, olive green, warm white, mushroom brown, and charcoal brown.

Trending colors:

- Sherwin-Williams Evergreen Fog

- Sherwin-Williams Pewter Green

- Benjamin Moore White Dove

- Benjamin Moore Pale Oak

- Sherwin-Williams Urbane Bronze

Landscaping Becomes More Organic

The “perfect manicured yard” is fading and leaning towards more organic landscapes. People want landscaping that feels connected to nature and has lower maintenance.

Trending:

- native plants

- meadow-style gardens

- layered greenery

- drought-tolerant landscaping

- edible gardens

- natural stone paths

Outdoor Living Rooms

Backyards are increasingly designed like interior spaces. Indoor-outdoor living was a big trend that was identified during Covid and stuck. It is still growing strongly, and a feature that creates expanded enjoyment and a great ROI when selling.

- outdoor kitchens

- lounge furniture

- fire pits

- pergolas

- textured lighting

- integrated dining spaces

The Overall 2026 Aesthetic

The big shift is from cold minimalism, gray everything, and ultra-modern perfection to warmth and layered texture that evoke emotional comfort by using nature-inspired materials, individuality, and timelessness. Designers are calling it organic modern, lived-in luxury, earthy vibrancy, and modern heritage. I hope this overview of the latest 2026 design trends has created some inspiration, whether you’re looking to make some minor, impactful tweaks or to embark on a remodel. Please reach out if you need access to some trusted vendors who can help you bring your vision to life.

Market Realities & Opportunities: Equity Growth, Improved Affordability & Overall Stability

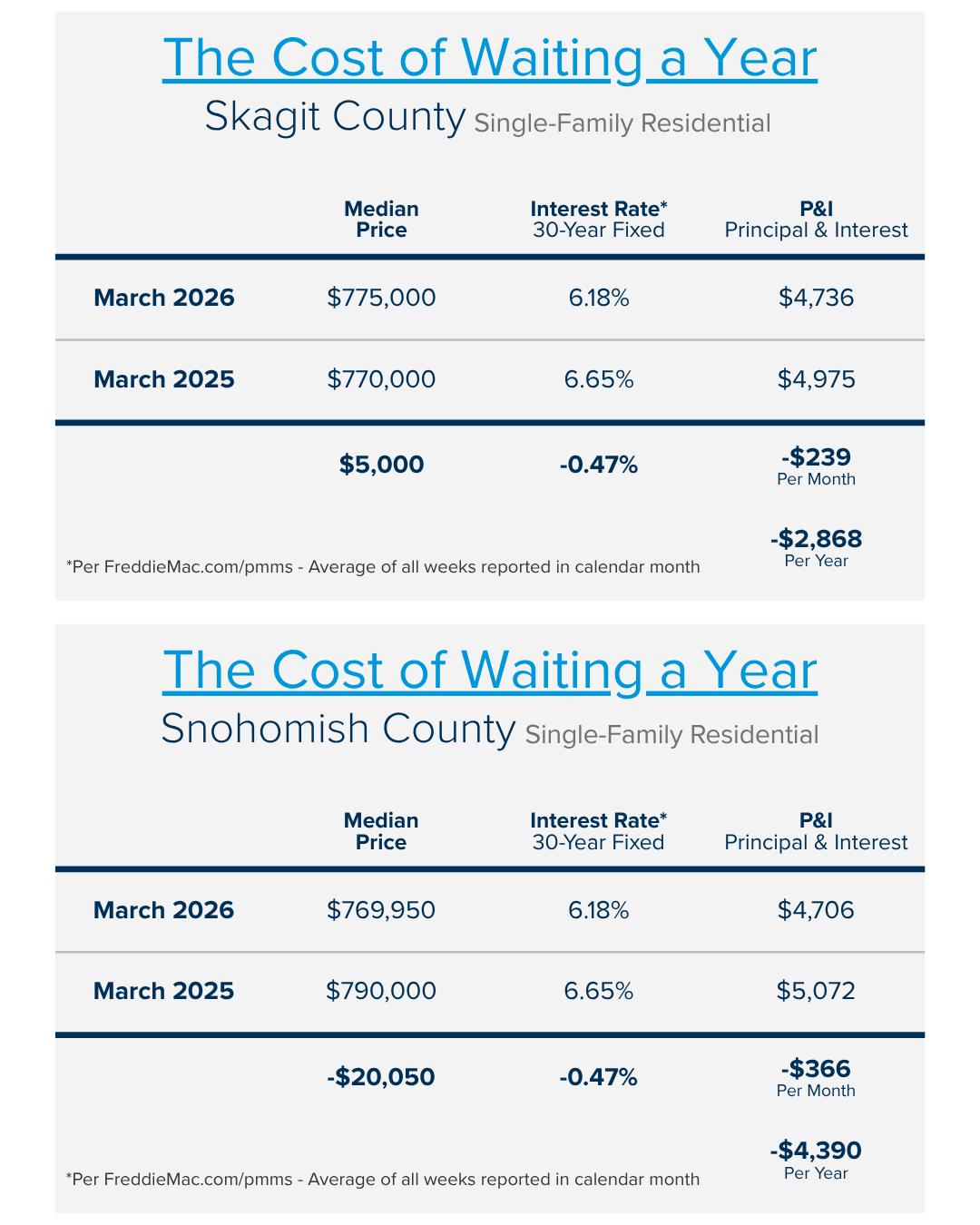

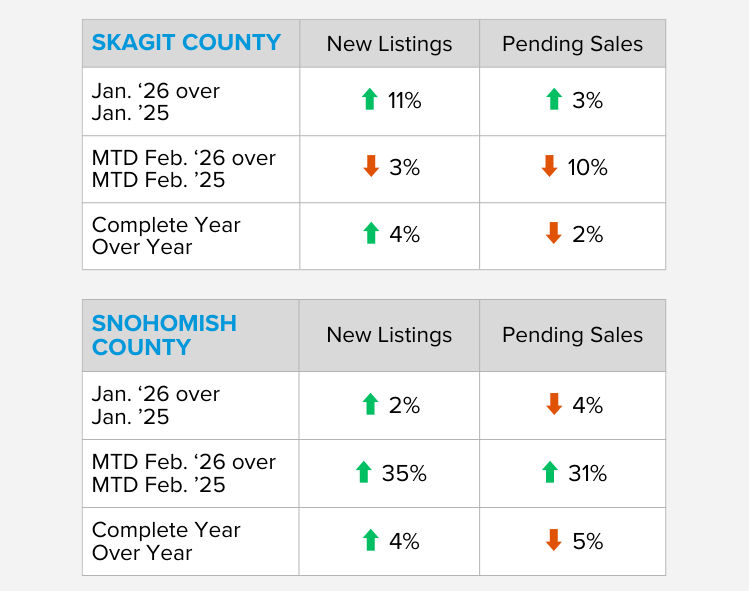

| With so many headlines about the housing market right now, I wanted to give you a clear, local, data-backed update, specifically breaking down what’s happening in Skagit and Snohomish counties. While the national conversation can feel uncertain, the local numbers tell a much more grounded story.

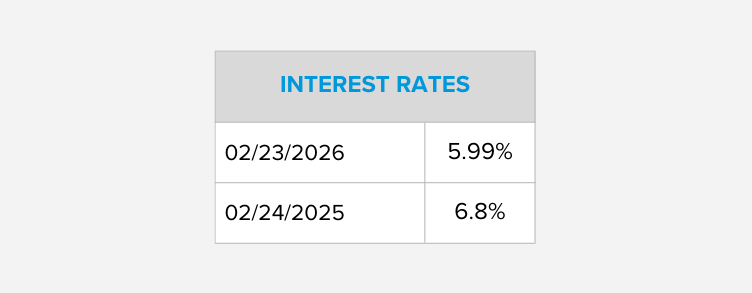

The biggest disruption we have experienced so far this year was the increase in interest rates since the US conflict with Iran began on February 28th. Let’s put this in perspective. Pre-conflict, rates hit 5.99%, the lowest they have been since the summer of 2022, and they quickly jumped to 6.59% by March 23, 2026, and on April 27th, 2026 settled around 6.3%. All in all, they took a quick jump up, but have seemed to settle over the last few weeks. While it was awesome to see 5.99% and the recent increase was disappointing, it’s important to also look back and understand that it is still more affordable to buy now compared to last year and the year prior. A year ago, on April 28th, 2025, rates were 6.83%, and on April 29th, 2024, they were 7.4%! This is a dramatic difference in favor of buyers now, coupled with flat prices year-over-year. Check out the charts below for both Skagit and Snohomish Counties for Single-Family Residential Homes, which show the real numbers surrounding monthly payments. |

|

|

|

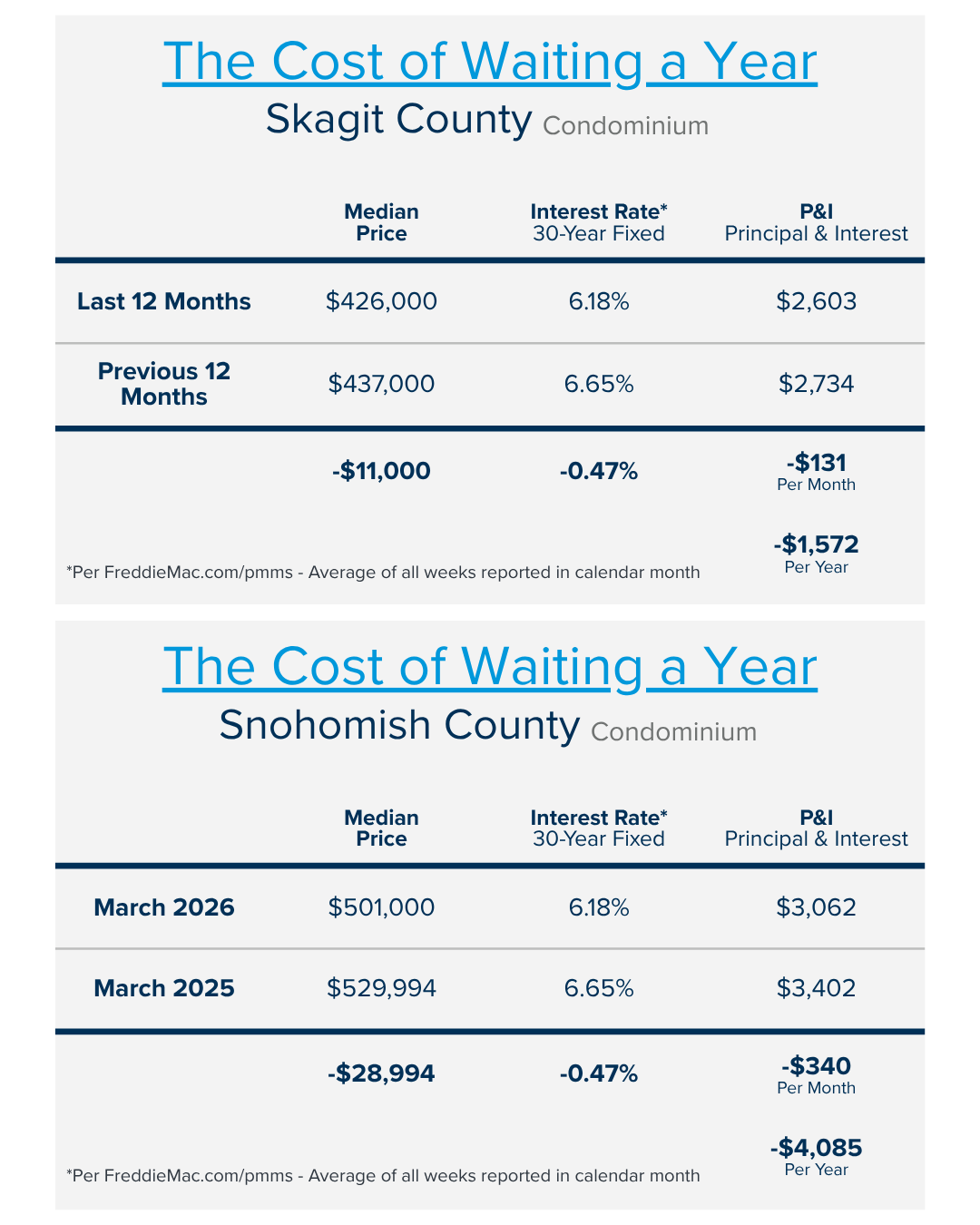

| With payments $239 lower in Skagit County year-over-year and $366 lower in Snohomish County, this is a welcome relief for buyers. Further, check out the charts below for the year-over-year savings for Condominiums: $131 and $340, respectively. This is especially beneficial for first-time homebuyers who will often purchase this property type based on affordability. | |

|

|

|

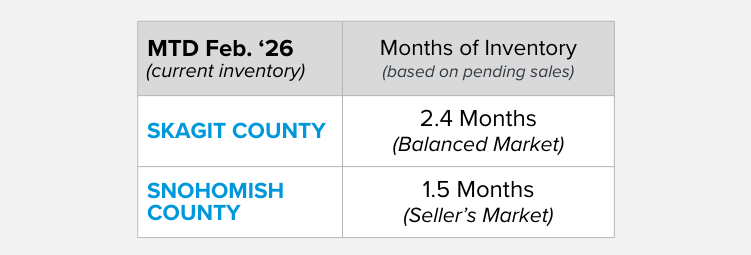

The Big Picture: Balanced Market in Skagit County & Still a Seller’s Market in Snohomish County Despite more inventory coming on the market, both counties are still competitive for Single-Family Residential Homes:

Inventory: Rising, But Not Oversupplied You may be hearing that inventory is “up”, and that’s true. Here’s what that actually looks like locally for Single Family Residential Homes: Skagit County:

Snohomish County:

What this means:

Home Prices: Stable! This is where headlines often get it wrong. Skagit County Single Family Residential:

Snohomish County Single Family Residential:

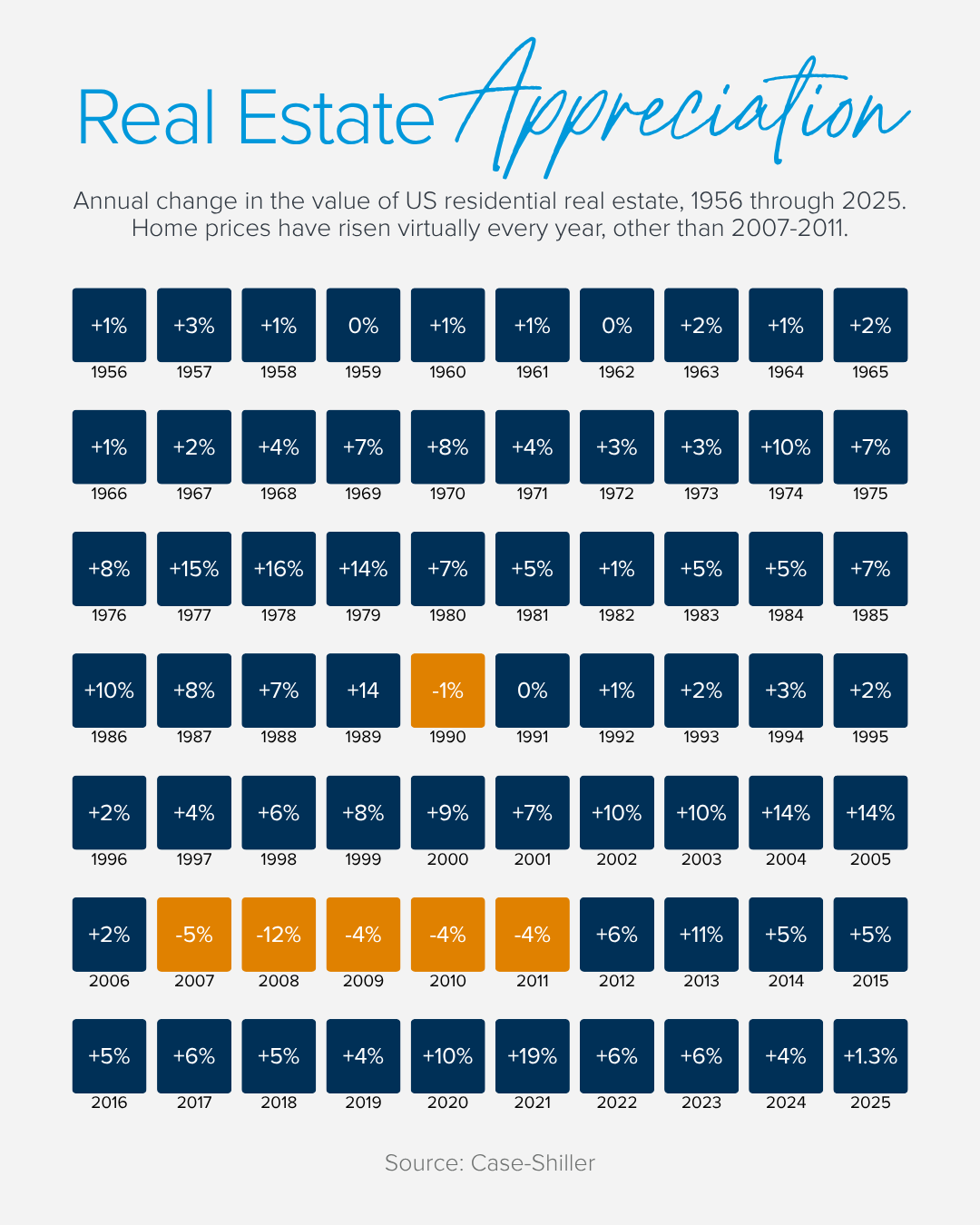

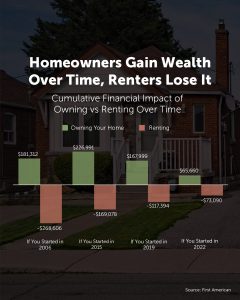

Key takeaway: This isn’t a declining market; it’s a normalizing one after rapid growth, with both counties still showing price stability. Home Equity is High, and Real Estate is a Proven Investment: The price growth for Single-Family Residential Homes since 2020 in Skagit County has been 54%, and in Snohomish County, 47%. Even more so, prices have increased 110% over the last 10 years in Skagit County and by 100% in Snohomish County. Further, check out this chart below, which shows the national figures on equity growth since 1956. Real estate has proven to be one of the best long-term investments a person can make, which leads to building strong household and generational wealth. |

|

|

|

|

Market Speed: Homes Are Still Moving Even with more inventory, homes are still selling at a steady pace:

And homes are still selling very close to asking:

Well-priced homes that are expertly prepared for market are the ones that are moving quickly and seeing less negotiations, especially in desirable neighborhoods. What This Means for You If you’re a buyer:

If you’re a seller:

Bottom Line The headlines may sound dramatic, but the local reality is much more balanced:

If you’re thinking about making a move, or just want to understand how this applies to your specific situation, I’m always happy to help you interpret the numbers. Please reach out if you’d like to learn more. I can apply these figures to your property type, location, and price point to help you understand the market more clearly. Clarity is key to empowering strong decisions, and I always lead with the data to provide sound guidance. |

What You Need to Know NOW: Real Time Trends for 2026 So Far (Skagit & Snohomish County)

A New Year always brings new energy to the real estate market, and 2026 is already starting to show signs of growth, more movement, and a return to normalcy. After three years of slower sales due to higher interest rates, homeowners not wanting to give up their historically low interest rates, and prices remaining stable, 2026 is starting to produce some positive results in the Greater Seattle area real estate market. Some key factors that I have been tracking since the calendar flipped to 2026 that show predictive trends are the rate of:

- New Listings

- Pending Sales (Real-Time Accepted Contracts)

- Cumulative Days on Market (CDOM)

- Sales Prices to Original List Price Ratios

- Months of Inventory (Is it a Seller’s, Balanced or Buyer’s Market?)

- Interest Rates

- Price Trajectory

One of the challenges we have faced over the last three years is a lack of inventory, with many would-be home sellers staying in their homes longer in order to hold onto their low rate and payment. This has led people to stay in homes that are not the best fit for their lifestyle, and this pent-up seller demand has started to break loose. As you can see from the chart above, New Listings are up in both King and Snohomish Counties year-over-year, especially this February. This shows that for some sellers, the time has come to focus on the right fit versus payment.

Additionally, another encouraging sign is an uptick in Pending Sales (Real-Time Accepted Contracts) year-over-year and most recently during the first two weeks of February compared to the same time last year. This illustrates that buyer demand is meeting the increase in new listings and that there is a ready and willing audience wanting more selection to choose from. When the increase in pending sales starts to pace and even outpace the rate of new listings, we know there is solid demand.

The most current data above for both King and Snohomish counties shows the Cumulative Days on Market (CDOM) for the current pending sales that were accepted since January 1, 2026; more than half quickly came off the market in two weeks or less! This is a stark difference from the CDOM for closed sales in January 2026, which most likely went pending (contract accepted) in late Q4 2025. The market is waking up to the New Year with vigor and excitement for well-prepared, appropriately priced homes.

The sales price to original list price ratios are also starting to improve, inching up to 98% in the first two weeks in February 2026 from 96% in January 2026. Home sellers that are aligning with a trusted advisor to help them prepare their home for market and stay close to the data for pricing are starting to see quicker, full-price sales, and in some cases, multiple offers with price escalations. It is important to note that property condition, cleanliness, expert staging and marketing, and realistic pricing all play a critical role in garnering optimal results.

This finds us currently (MTD February 2026) in a Seller’s Market based on pending sales (0-2 Months of Inventory) in both King and Snohomish counties after only being 45 days into 2026. We calculate Months of Inventory by dividing the number of pending sales by the number of available homes for sale to determine how quickly we’d run out of inventory if no new homes came to market based on pending sales demand. We have not been at this level since April 2025 and spent the remainder of 2025 in a balanced market, so this is a marked improvement.

Interest rates are almost an entire point lower than they were last year at this time, which affords a buyer 10% more in buying power or simply results in a lower payment at the same sales price. You can view the video from Jeff Tucker, Windermere’s Chief Economist, below on what has caused interest rates to decrease. Rates declining closer to 6% and teetering towards the high 5% will unleash more demand in the market as it makes homes more affordable, and with prices maintaining, the rate matters! I think this has also led more potential home sellers to come to market as the current rates are more palatable than when they were 1-2 points higher over the last three years.

This brings us to price trajectory. With eight months of 2025 being a balanced market, rates hovering in the 7% throughout last year, and many of the homes that closed in January 2026 going under contract in late 2025, January prices recorded at lower price levels. When you take the median price over the last 12 months and compare it to the previous 12 months (complete year-over-year), prices are flat and stable.

With early indicators such as pending sales, lower rates, and faster CDOM, I anticipate more historical price growth levels in 2026, between 3-5%. I certainly do not anticipate prices lowering. In fact, we have seen list prices soften, and more home sellers who are truly motivated come to market with realistic expectations and better market preparation. The new normal is taking shape.

This uptick in market activity and return to normalcy comes on the shoulders of extreme home equity growth since 2020 and over the last 10 years. The growth is staggering! The abundance of wealth that people have in their homes is beneficial to positioning a move that better fits their lifestyle, funding a remodel, helps plan for retirement, or even an out-of-state move as long at the payment works. The recent decrease in rate and long-term equity gains have supported these exciting moves.

If you or someone you know are curious about how the latest trends, long-term growth in the market, and current rates affect your ability to make a move, please reach out. I am committed to staying close to the real-time data, assisting with discerning the information, and applying it to my clients’ goals to help them navigate big life changes. It is my mission to help keep my clients informed, so they are empowered to make strong decisions. 2026 is already starting to provide some great opportunities, and if you’d like to learn more, let’s talk!

Top 5 HYPER-LOCAL 2026 Predictions & Takeaways – Skagit County

Earlier this month, my office hosted Matthew Gardner where he shared clarity, context and hyper-local insight during a time when many people are craving grounded information. Thank you to Matthew Gardner for sharing his expertise, and to those of you who joined the event live. If you weren’t able to attend, I’m glad you’re here as below are my key takeaways, with a deeper focus on Skagit County.

|

Skagit County:

-

Inventory: Expected to grow more meaningfully, giving buyers increased selection

-

Sales: Forecast to improve modestly as affordability and inventory align more favorably

-

Prices: Anticipated to experience slow, steady growth rather than sharp increases

Matthew highlighted Skagit County as an area that continues to benefit from relative affordability, especially for buyers priced out of neighboring markets.

Final Thoughts

Matthew summarized the market as one that is adjusting, not unraveling.

-

Prices are not falling

-

Demand has not disappeared

-

The market is becoming more balanced and less frantic

For homeowners, this means long-term equity remains intact.

For buyers, it means more opportunity to move thoughtfully rather than urgently.

If you’d like help interpreting how these trends apply to your specific neighborhood, property type, or goals, I’m always happy to walk through the data with you.

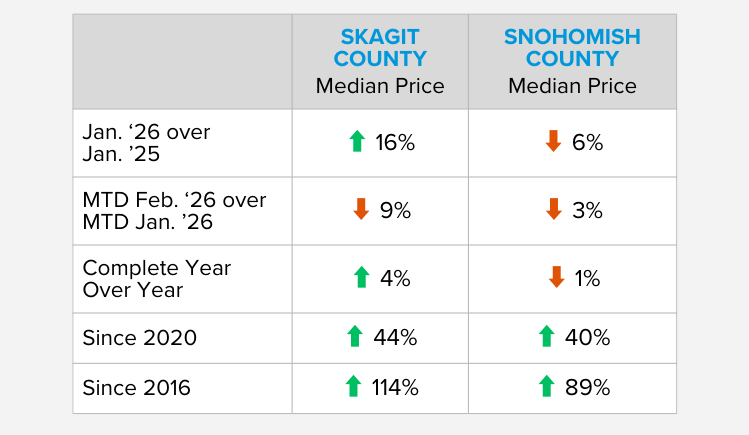

Market Check: Skagit County January 2026

📊 January Market Snapshot | Skagit County

The year is starting with momentum.

✔️ Median price: $665,000 (⬆️ 16% year over year)

✔️ New listings up 95% over December

✔️ Pending sales up 43% over December

✔️ Inventory at just 2.3 months

And here’s what really matters ➡️ interest rates are lower than this time last year (6.13% vs 7.04%).

What does this mean?

Buyers: More options are coming online, and rates are improving, but inventory is still tight. Strong homes are moving.

Sellers: Demand is active and prices are holding. Strategic pricing still matters.

January is often a signal month for the rest of the year… and this one is telling us the market is awake.

If you want to know what this means for your neighborhood or price point, message me.

The North Cascades

Wild Beauty Meets Endless Wonder in the North Cascades. If you have ever taken Highway 20 or stood at a lookout along the North Cascades Scenic Byway, you have experienced the difference. It is more dramatic, raw, and rugged than just about anywhere else in Washington. What makes The North Cascades so different? They aren’t just mountains! They are one of the most spectacular landscapes in North America. The product of being carved by ice, shaped by time, and wrapped in a sense of wildness that is difficult to describe but impossible to forget once experienced.

Welcome to the North Cascades: the “American Alps” that live up to their name in every way.

A Landscape Carved by Time and Ice

The North Cascades are some of the most rugged mountains in the continental United States. There’s a reason for that! For millions of years, glaciers have scraped, sculpted, and carved this region into sharp ridgelines, jagged peaks, plunging valleys, and steep-walled canyons.

It’s this geologic history that gives the range its dramatic appearance:

- Craggy peaks that cut into the sky

- Deep turquoise lakes fed by glacial runoff, like Diablo Lake

- U-shaped valleys formed by massive sheets of ice

- Waterfalls that appear to tumble from nowhere

Counts cite over 300 glaciers! For reference, North Cascade glaciers make up nearly a third of all glaciers found in the lower 48 states. By far, the largest collection in the Lower 48. These glaciers continue shaping the landscape today, leaving behind the striking blues and rocky textures the North Cascades are known for.

A Wilderness of Pines, Snow, and Untamed Beauty

The North Cascades are home to dense forests of cedar, fir, and pine that cling to the slopes and fill the valleys below. As you approach the higher elevations, the trees give way to wildflower meadows, windswept ridges, and snowy peaks that remain frosted long into summer.

It is here; you find:

- Towering evergreens that fill the air with the scent of resin and rain

- Snowfields and glaciers that glow blue in the afternoon light

- Wildlife like black bears, marmots, mountain goats, and soaring eagles

- Alpine lakes so clear that they reflect the peaks like glass

The North Cascades are remote enough to feel untouched, yet accessible enough that anyone can experience moments that feel like pure wilderness escape.

The North Cascades Highway: A Drive Like No Other

If there is one thing that elevates this mountain range even further, it’s the drive.

Highway 20 (the North Cascades Scenic Byway) is often called one of the most beautiful drives in the country. For good reason, every switchback and overlook reveals something new:

- The emerald waters of Diablo Lake

- The towering spires of Liberty Bell Mountain

- The vast, layered ridgelines stretching endlessly into the horizon

- Rivers, forests, and valleys that change color with every season

Whether you are stopping at lookouts, hiking a trail, or simply soaking in the view from your car window, the drive offers a sense of awe that builds mile after mile.

Fall lights up in fiery colors of oranges and golds. Winter wraps the peaks in white. Spring returns with roaring waterfalls, and summer unveils the full glory of alpine blue skies. No matter when you visit, the North Cascades feel like a new place every time.

What Makes the North Cascades So Special?

It’s a combination of drama, solitude, and sheer natural beauty. It is the feeling of seeing mountain after mountain fade into the distance, knowing most of them are untouched wilderness. It’s the sense that the land is old, powerful, and yet still shaping itself.

The North Cascades are special because they remind us of something rare:

There are still places where nature feels truly wild.

Thinking about calling the PNW home? Let’s Connect!

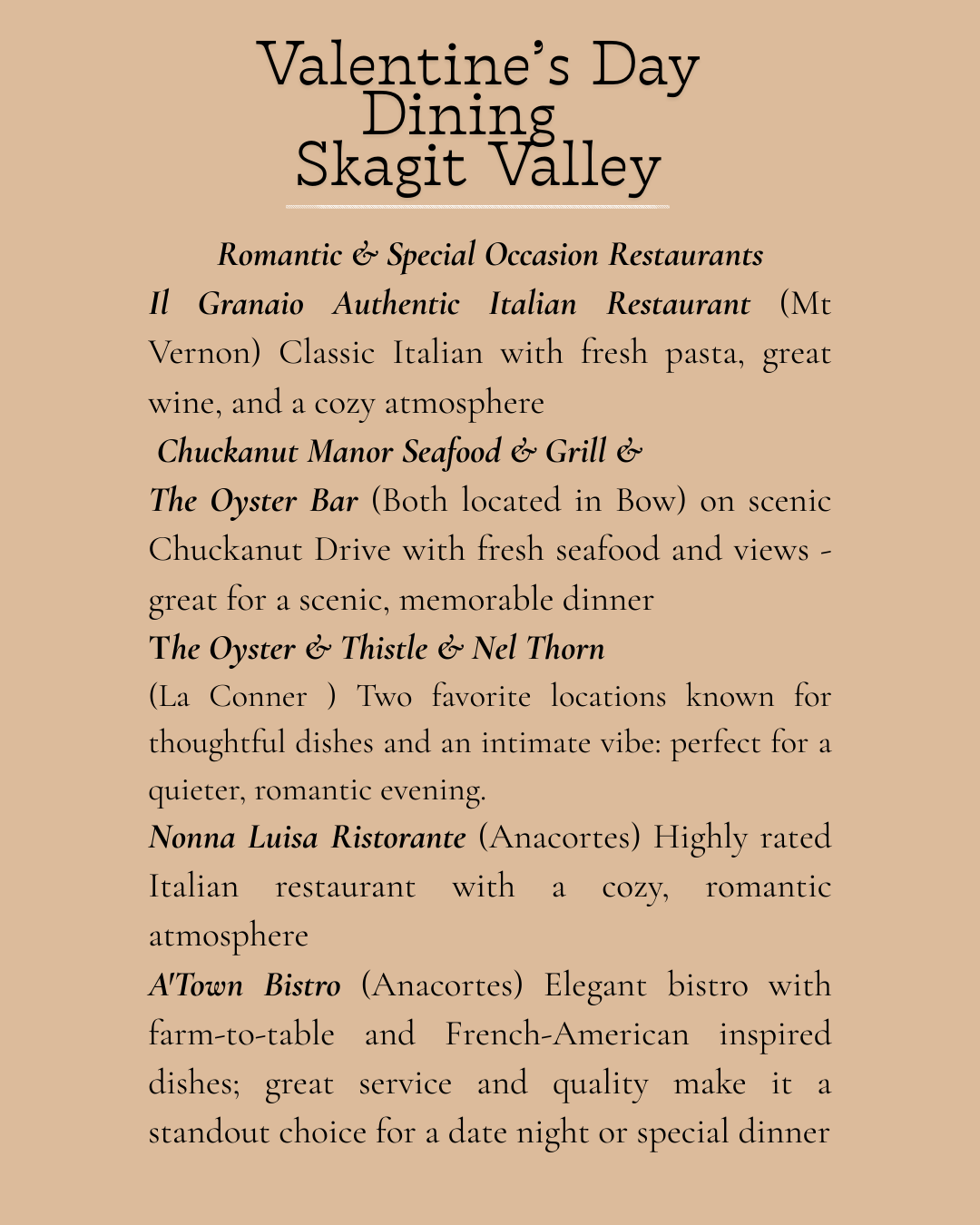

February in the Skagit Valley

And just like that… hello February 💕

The shortest month of the year, but packed with ALL the cozy vibes, sweet treats, and local fun here in Skagit County.

From Valentine’s dinners (book early) to community happenings, I’ve rounded up some favorite ways to love local this month. 💌

Share this blog with your favorite date night buddy or adventure partner below! Hope to see you out and about around town. 😊

Your Skagit County Realtor, sharing local favorites + all things home. 🤍

Home Updates That Actually Pay You Back When You Sell

Planning to sell this spring? While you may be tempted to hold off until the first blooms or the spring showers hit, that’s actually waiting too long to get started by today’s standards.

Buyers have more options than they did a few years ago. So, it’s worth it to tackle repairs now and make sure your house is set up to stand out. Because you don’t want to be caught scrambling right before the spring rush. Or, running out of time to do the work your house really needs.

The key is focusing on updates that actually matter. And that’s exactly where return-on-investment (ROI) data comes in handy.

Which Projects Tend to Pay Off?

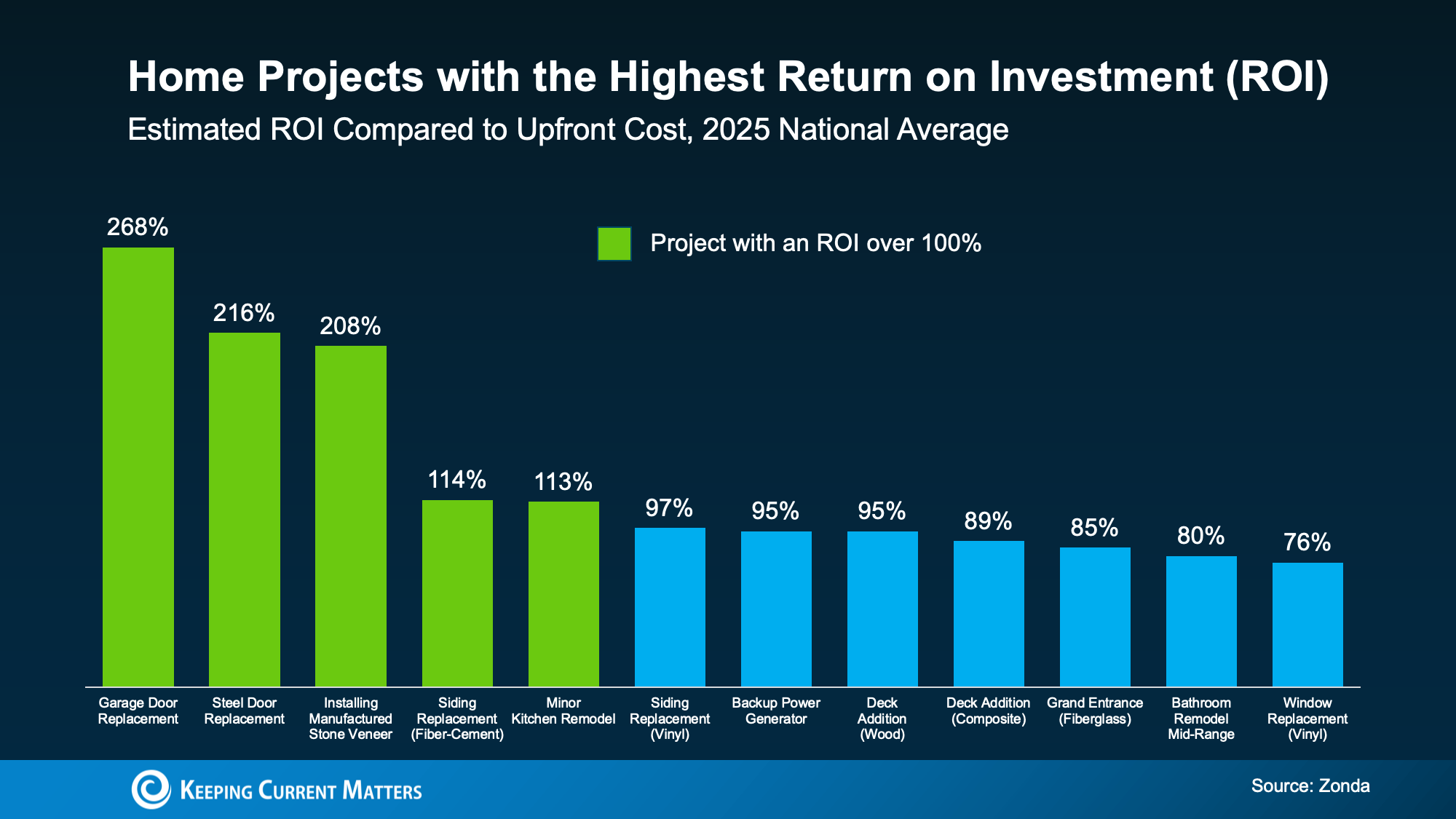

Every year, Zonda looks at which home improvements deliver the most bang for the buck when you go to sell the home. And the results can be a little surprising.

The green in the chart below shows the updates where sellers have the biggest potential to add value based on that research:

While there’s a wide range of projects represented in this data, the cool part is, some of the top winners aren’t big to-do’s. They’re just swapping out doors.

Small Updates, Big Visual Impact

This goes to show little projects can have a big impact. So, you don’t have to spend a fortune. And you don’t need to tackle everything on this list. But in today’s market, doing nothing can work against you.

Now that buyers have more homes to choose from, a lot of them are going to opt for what’s move-in ready.

The best advice? Focus on what your house needs, whether it’s listed here or not – like the repairs you’ve been putting off. A front door or shutters in need of a little TLC. Piles of leaves in the yard. Scuffed up paint where your kids play inside. Those details matter too.

Mallory Slesser, Interior designer and Home Stager, explains it to the National Association of Realtors (NAR) this way:

“If you’re looking for affordable updates that pack a punch, dollar for dollar, I would say painting; changing out light fixtures; changing out hardware; maybe new draperies or window treatments. Those are all cost-effective ways to make a big statement. It really changes the space.”

These seemingly small things help buyers focus on the home itself – not the work they think they’ll have to do after moving in. And that’s paying off for other sellers. Buyers are often willing to spend more on homes that feel well cared for, updated, and move-in ready.

Here’s the important thing to remember. National data like this is a guideline. Buyer preferences are going to vary by location, price point, and even neighborhood. That means a project that boosts value in one area might be unnecessary (or even overkill) in yours. I’m Danielle Martin, and I help clients understand which investments deliver the strongest ROI in the North Sound and throughout the Pacific Northwest

Affordability Strategies – House Hacking Tips to Help Overcome Monthly Payment Barriers

While we are seeing the market show signs of improvement and uptick in activity in Q4 2025, the biggest challenge we see in the real estate market is affordability. Prices in our area have remained stable after many years of appreciation, and interest rates, while improving, are hovering around 6.25%. This combination has monthly payments expensive, especially for first-time buyers and buyers on fixed incomes, such as retirees, seniors, or people looking to retire and fix their overhead.

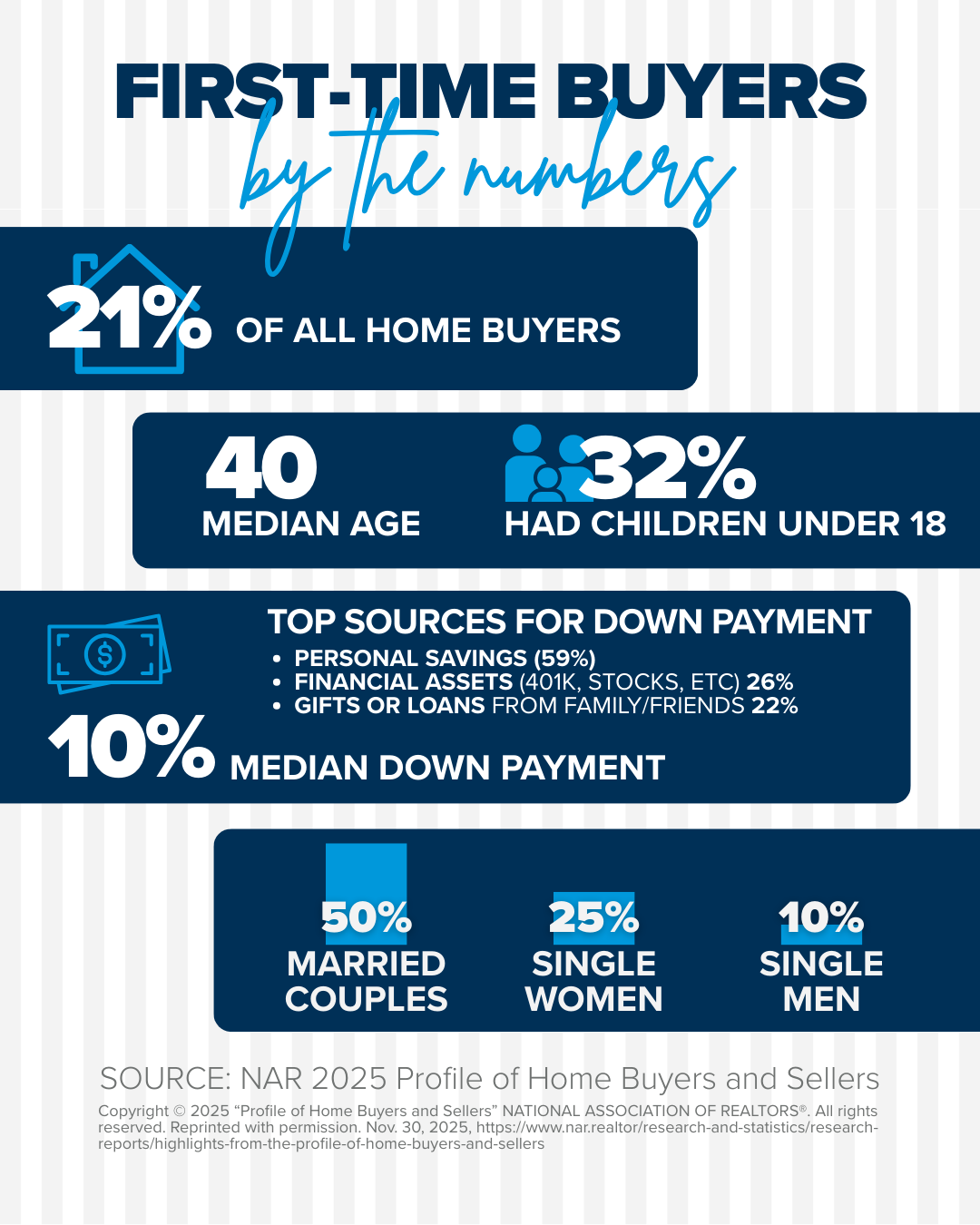

In fact, the latest Profile of Homes Buyers and Sellers by the National Association of Realtor (NAR) shows that the rate of first-time buyers is at an all-time low, accounting for only 21% of all buyers. The median age for this group increased to age 40, the highest ever. This illustrates that affordability is putting pressure on this group and delaying their start to building long-term household wealth. The average net worth of a renter versus a homeowner is staggering, so this is an important obstacle to overcome for those who have the resources but find themselves on the bubble of this decision.

I have helped buyers overcome affordability challenges by applying some creative house hacking strategies. These are powerful tools, as they can empower a person to become a homeowner instead of renting, putting them on the path to building household wealth much faster. Plus, Greater Seattle Area rents are costly, so if one can find a way to pay their own mortgage instead of their landlord’s, they will start to build a nest egg of security for their own future.

A common myth we see is that buyers think they need 20% down to buy a home. That is simply not true, according to NAR, the average down payment for a first-time buyer was 10%. While a 20% down payment can eliminate mortgage insurance, there are loan programs such as FHA and some Conventional programs that only require 3-5% down. There are also down payment assistance programs that are available that result in 0% down, and VA financing can be as low as 0% as well.

Speaking of down payments, I see buyers diversify by utilizing or borrowing against stocks and/or 401K funds, and the NAR survey revealed 26% of first-time buyers used these types of funds to achieve their homeownership goals. It is also not uncommon for some fortunate buyers to receive gift funds in order to achieve homeownership, and the NAR survey showed 22% of first-time buyers were able to utilize this route. With the big picture of building household wealth in mind and the fact that everyone needs a roof over their head, having your home be a part of your investment portfolio makes sense.

House Hacking Tips for First-Time Buyers

The “Live in One, Rent the Rest” Starter Play

Shop 2–4 unit properties (duplex/triplex/fourplex). When you buy a multi-unit property and live in one unit, you get to enjoy owner-occupied financing rates. You can live in one of the units and rent the other(s) to help offset your mortgage payment. This could even allow for a lower down payment. It is important to calculate your potential monthly payment and assess rental rates in the area to figure out how having a renter(s) would help offset your monthly overhead. Also, consider if you had a vacancy, could you still make it work while you tried to fill it.

If the numbers work for your monthly cash flow, this is an excellent way to obtain homeownership. Down the road, you are building equity while someone else helps pay down your mortgage. Further, if you wanted to eventually move on to another property, you could sell this and reap the equity for a larger down payment or keep the property (at the owner-occupied financing rate) and rent all the units.

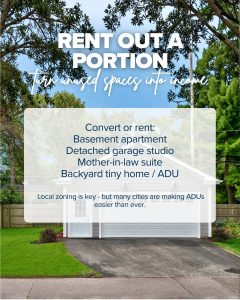

ADU Options

Seattle allows up to two ADUs per lot, and no owner-occupancy requirement (you don’t have to live there forever to keep it legal). Parking requirements are relaxed, too. Outside of Seattle these zoning requirements vary, but this is a rising trend.

You could buy a home with an existing ADU (detached cottage, basement unit, garage studio). Or buy an “ADU-ready”: daylight basement + exterior door, or garage with alley access. Start by renting a room or partial suite now, then add/finish an ADU later when cash allows.

Rent-by-the-Room to Offset Overhead

One roommate can take the edge off your payment; two roommates can be a full-on subsidy. When shopping for a home, prioritize layouts that naturally separate space (split-levels, basements, mother-in-law setups). I’ve seen some buyers already know who their roommate will be, so they can shop with confidence and also be comfortable with their living situation.

Purchase with a Trusted Partner with Similar Housing Goals.

Pooling funds for a down payment and sharing the monthly overhead is a great way to obtain homeownership with a trusted partner. This could be a close friend, family member, or domestic partner. You would ideally need to commit to at least 3-5 years of sharing the mortgage to build equity and avoid selling too early, and having a written agreement outlining the exit strategy is key. Based on average annual appreciation rates, 3-5 years would offset any selling costs and provide equity growth outside of something catastrophic happening in the market. This is a great way to protect your savings, build wealth as a team, and not throw money away on rent.

I knew two young women who pooled their savings to buy a home, and they also placed a roommate in a basement bedroom to help offset the mortgage. They later sold that house when they both got engaged and were able to buy great long-term homes with their partners using the equity they built. This partnered approach on their first home put them on the path to stability, security, and flexibility for their futures.

Buy a Cosmetic Fixer

Many buyers prefer homes that are “done” and fully updated. Those homes often come at a premium because they have a larger buyer audience. If you are willing to live with dated finishes or an unfinished space, you have the opportunity to build sweat equity with improvements you can make down the road when you can afford to.

It is important that you look for a home that’s structurally sound, as those can be expensive items to remedy, such as electrical, plumbing, roof, etc. Hiring a trusted inspector to perform proper due diligence is an important step. A dated kitchen or bathroom is a livable situation, and these homes build equity over time, too. If a home has an unfinished basement, there is an amazing opportunity to finish that space in the future and gain a higher value. Plus, you could rent this finished space to help offset the expense.

Buy a Fixer

There are renovation loans available, such as an FHA 203(k), that can be used to do more extensive repairs, additions, and updates. These loans provide funds to make improvements after closing. They are very detailed loan programs that require further scrutiny on value through appraisal and contractor bids, but can be successful in bringing a broken-down home to a livable structure and on the path to building equity. You have to be hearty and resourceful for these projects, so heed caution when considering this option. I have a great list of vendors and contractors that can help.

Most importantly, you must consider the Triangle of Buyer Clarity when shopping. Whether you are house hacking or just buying your first home without any of these creative solutions, being realistic about what you can afford is paramount. The relationship between location, price, and features/condition matters! Buyers must be flexible with their wants and understand that in reality, they typically get 70-75% of what’s on their wish list. Such as buying a townhome instead of a single-family home, settling on a location a little further away, or choosing a home that is not perfectly updated. However, they get a house and an opportunity to build wealth! This wealth-building game is a step-by-step process with every home a stepping stone over time.

As you can see, this triangle is not a perfectly balanced triangle, some sides are adjusted more than others. A buyer may have to reduce the number of features they would like in order to obtain the price and/or location they desire. This gets them on the path of equity growth, though, so compromise and flexibility are key! You need to get clear on your goals and adjust the triangle to make it work.

If you are curious about how these house hacking tips can help you or someone you know, or you’re just curious about the market, please reach out. It is always my goal to help keep you informed in order to empower strong decisions.