Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

A Record Percent of Buyers Are Planning To Move in 2025 – Are You?

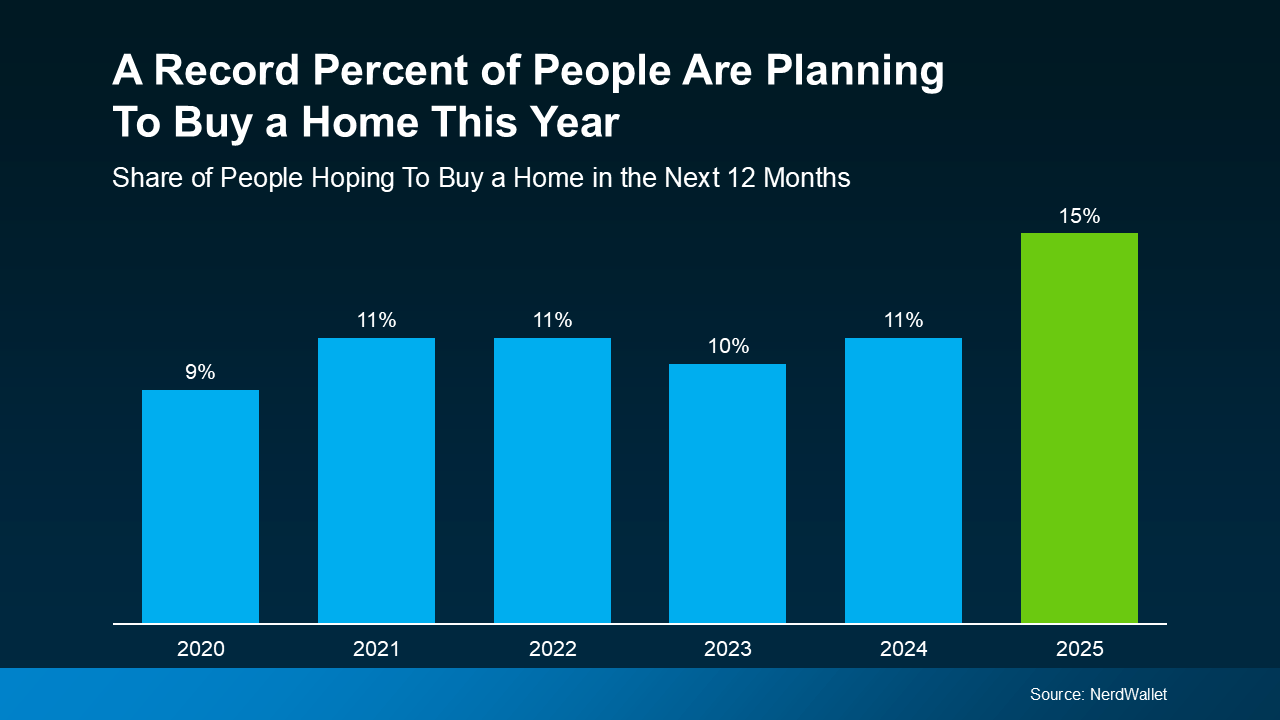

This could be the year to sell your house – and here’s why. According to a recent NerdWallet survey, 15% of people are planning to buy a home this year. That’s actually a record high for this survey (see graph below):

Here’s why this is such a big deal. The percentage has been hovering between 9-11% since 2020. This recent increase shows buyer demand hasn’t disappeared – if anything, it indicates there’s pent-up demand ready to come back to the market.

Here’s why this is such a big deal. The percentage has been hovering between 9-11% since 2020. This recent increase shows buyer demand hasn’t disappeared – if anything, it indicates there’s pent-up demand ready to come back to the market.

That doesn’t mean the floodgates are opening and that there’s going to be a huge wave of buyers like we saw a few years ago. But this does signal there’ll be more activity this year than last.

At least some of the buyers who put their plans on hold over the past few years will jump back in. Whether they’re feeling more confident about moving, they’ve finally saved up enough to buy, or they simply can’t wait any longer – this is the year they’re aiming to take the plunge.

And, according to that same NerdWallet survey, more than half (54%) of those potential buyers have already started looking at homes online.

That’s a good indicator that a number of these buyers will be looking during the peak homebuying season this spring. So, if you find the right agent to make sure your house is prepped, priced, and marketed well, you can get your house in front of them.

More people are going to move this year, and with the right strategy, you can make sure your house is one of the first they look at.

What do you think these buyers will love most about your house?

Let’s talk it over and make sure it’s front and center in your listing.

3 Reasons To Buy a Home Before Spring

3 Reasons To Buy a Home Before Spring

Let’s face it — buying a home can feel like a challenge with today’s mortgage rates. You might even be thinking, “Should I just wait until spring when more homes hit the market and rates might be lower?”

But here’s the thing, no one knows for sure where mortgage rates will go from here, and waiting could mean facing more competition, higher prices, and a lot more stress.

What if buying now — before the spring rush — might actually give you the upper hand? Here are three reasons why that just might be the case.

1. Less Competition from Other Buyers

The winter months tend to be quieter in the real estate market. Fewer people are actively looking for homes, which means you’ll likely face less competition when you make an offer. This makes the process feel less rushed and less stressful.

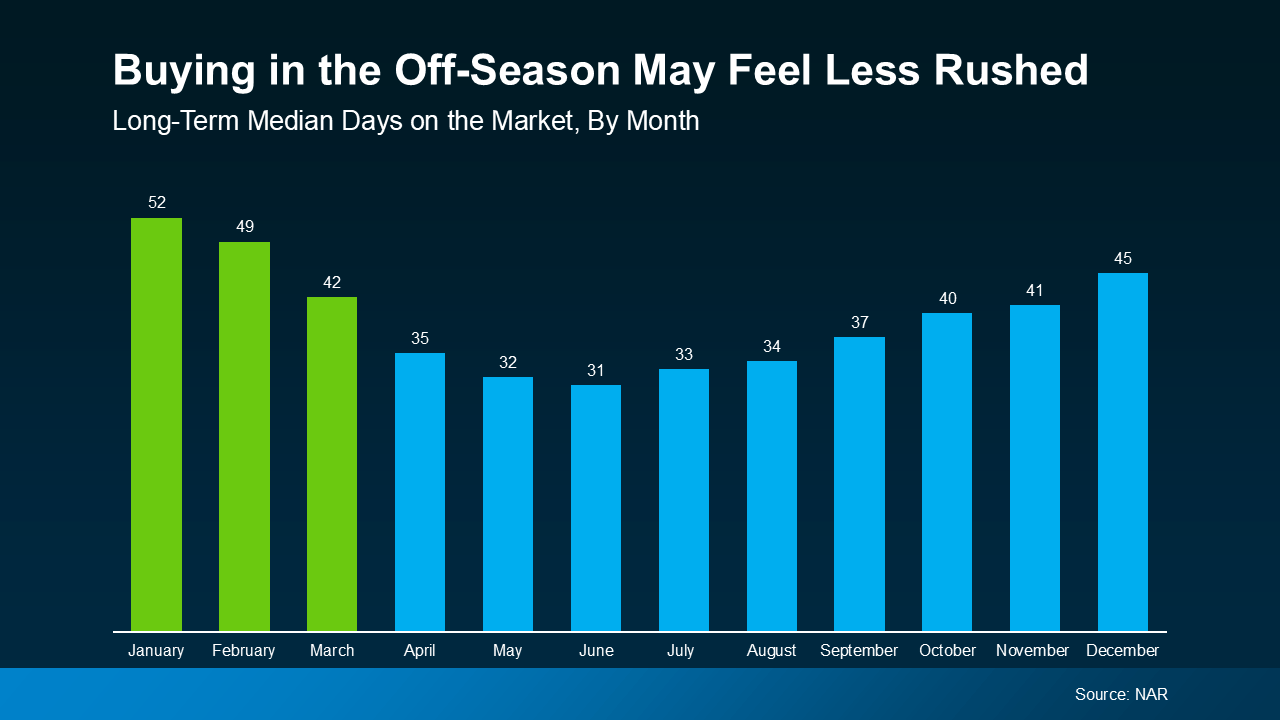

According to the National Association of Realtors (NAR), homes sit on the market longer in winter compared to spring and summer (see graph below):

Fewer buyers in the market means you’ll likely have more time to make thoughtful decisions. It also means you may have more negotiating power. According to the Alabama Association of Realtors:

Fewer buyers in the market means you’ll likely have more time to make thoughtful decisions. It also means you may have more negotiating power. According to the Alabama Association of Realtors:

“A significant benefit of buying a home in winter is the reduced competition. Because of the perceived benefits of spring, many buyers delay the start of their house hunt. As a result, you will find fewer people competing for the same properties during winter. Less demand can translate into more negotiating power as sellers may be more willing to entertain offers or agree to concessions to get a deal closed quickly.”

2. More Negotiating Power

With homes staying on the market longer, sellers may be more willing to negotiate. This can lead to better deals for you as a buyer, whether that means a lower price or added incentives, like sellers covering closing costs or making repairs. As Chen Zhao, an Economist at Redfin, points out:

“. . . buying during the off season means less competition from other buyers. That means potentially negotiating a better deal.”

Plus, when demand is lower, sellers often feel more pressure to work with serious buyers. This could give you an edge to negotiate terms that work best for your situation.

3. Lock in Today’s Prices Before They Rise

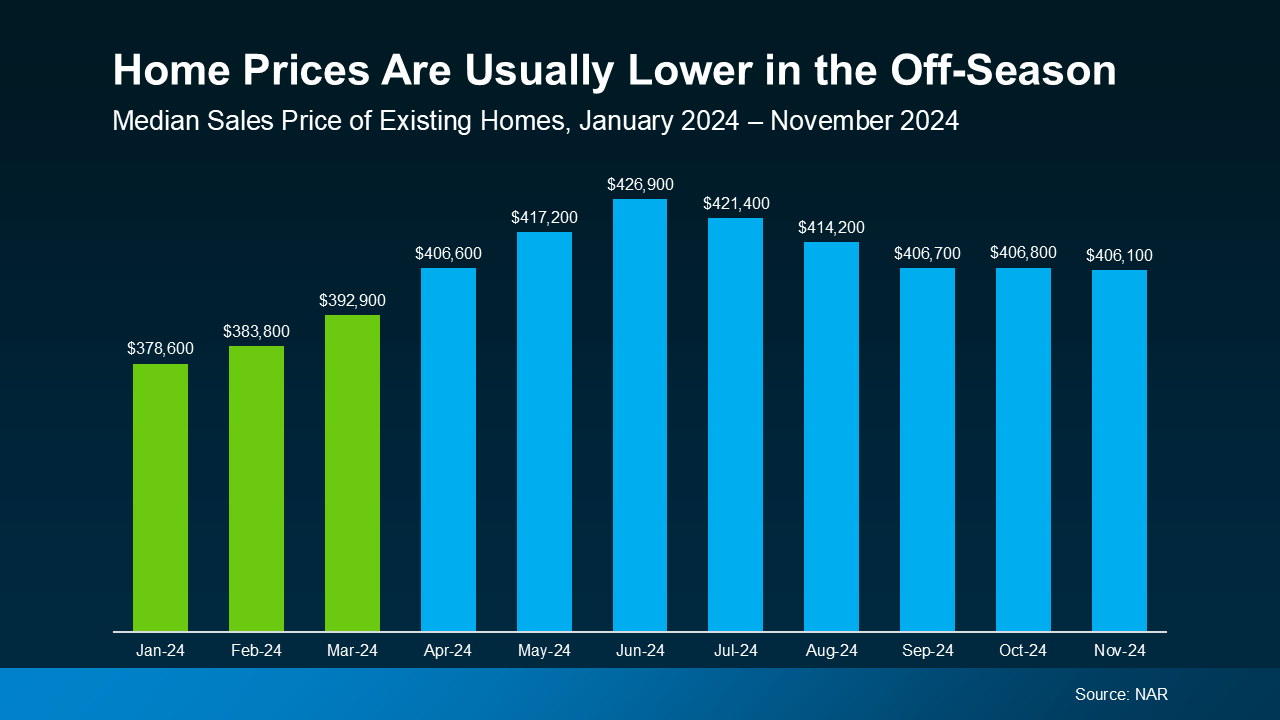

Historically, home prices tend to be at their lowest point in the winter months, too. According to data from NAR, home prices last year were at their lowest in January, February, and March — right before the spring buying season kicked in (see graph below):

This trend isn’t new — Bright MLS shows between 2010 and 2024, home prices in January and February were, on average, 15% lower than during the month of peak home prices (typically June). Buying in the off-season means you’re more likely to avoid paying the premium prices that come with the high demand of spring.

This trend isn’t new — Bright MLS shows between 2010 and 2024, home prices in January and February were, on average, 15% lower than during the month of peak home prices (typically June). Buying in the off-season means you’re more likely to avoid paying the premium prices that come with the high demand of spring.

On top of that, home prices generally appreciate over time, meaning they tend to go up year after year. That means if you’re ready to buy and you can make it happen, you’re not only taking advantage of what might be the lowest prices of the year, but you’re also locking in today’s price before it increases in the future.

Bottom Line

While spring may seem like the obvious time to buy, moving before the peak season can give you significant advantages, like less competition, more negotiation power, and lower prices.

If you’re ready to explore your options, let’s connect.

Time in the Market Beats Timing the Market

Trying to decide whether it makes more sense to buy a home now or wait? There’s a lot to consider, from what’s happening in the market to your changing needs. But generally speaking, aiming to time the market isn’t a good strategy – there are too many factors at play for that to even be possible.

That’s why experts usually say time in the market is better than timing the market.

In other words, if you want to buy a home and you’re able to make the numbers work, doing it sooner rather than later is usually worth it. Bankrate explains why:

“No matter which way the real estate market is leaning, though, buying now means you can start building equity immediately.”

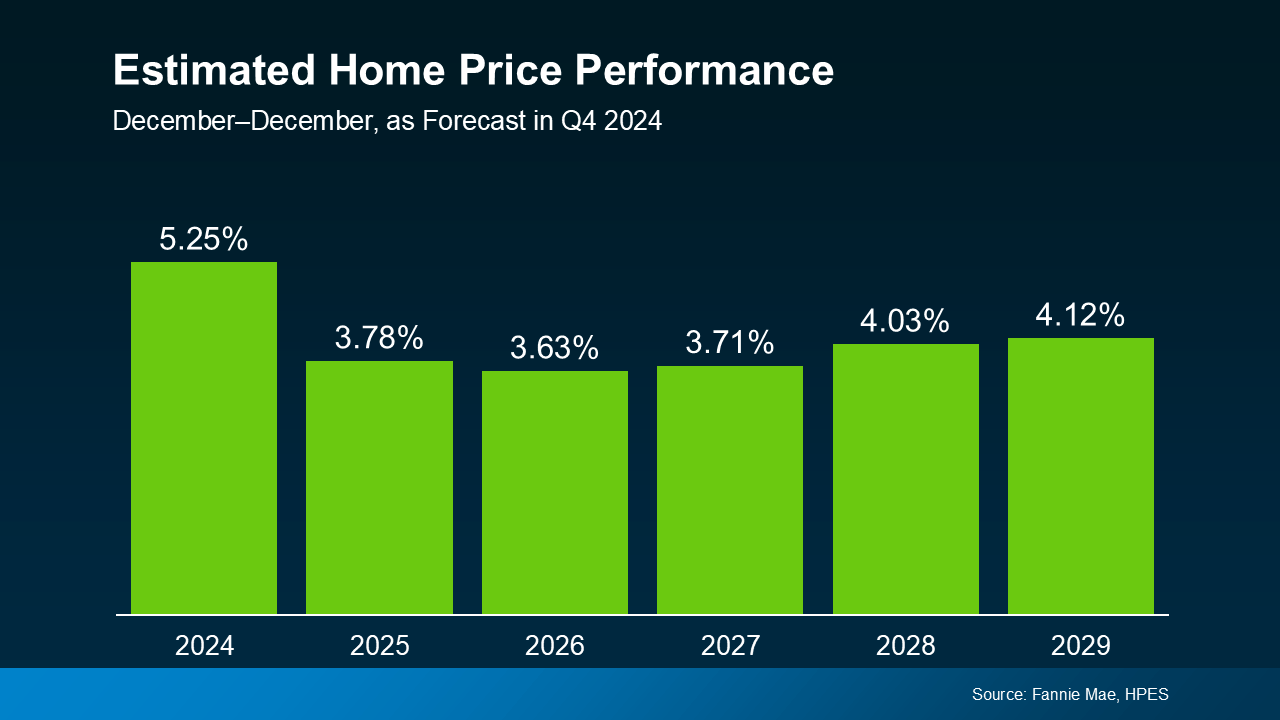

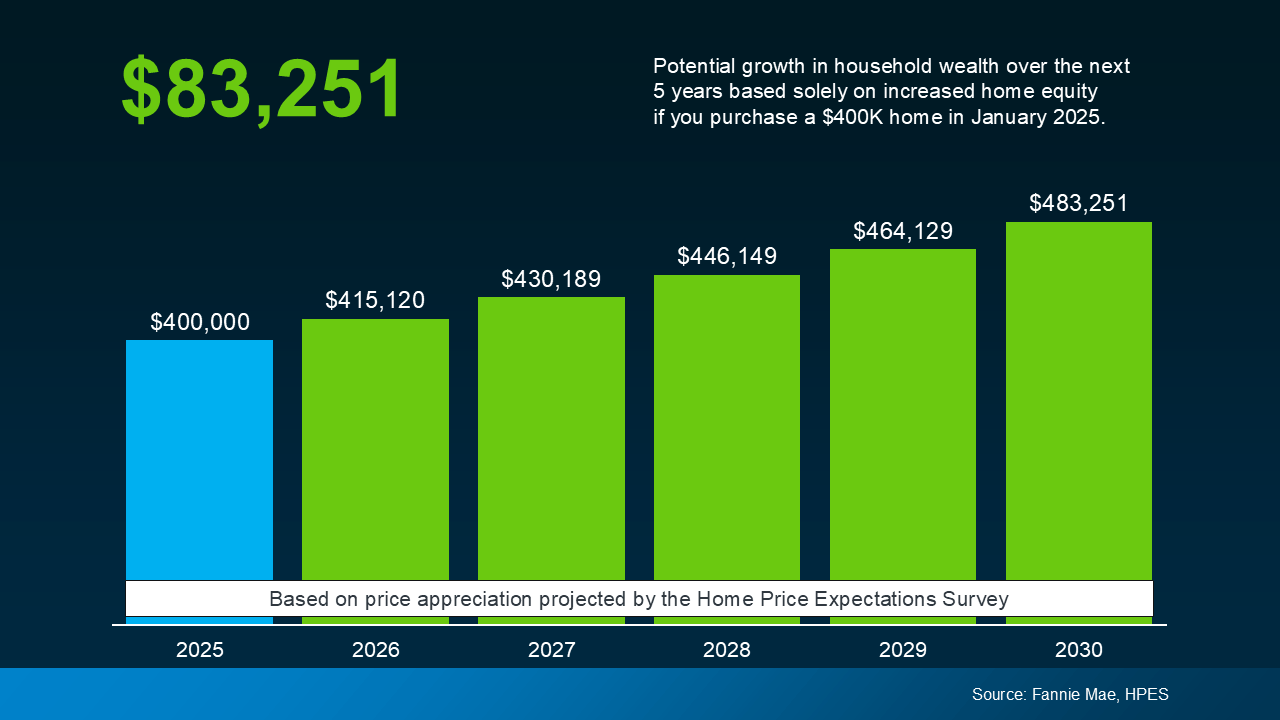

Here’s some data to break this down so you can really see the benefit of buying now versus later – if you’re able to. Each quarter, Fannie Mae releases the Home Price Expectations Survey. It asks over one hundred economists, real estate experts, and investment and market strategists what they forecast for home prices over the next five years. In the latest release, experts are projecting home prices will continue to rise through at least 2029 – just at a slower, more normal pace than they did over the past few years (see the graph below):

But what does that really mean for you? To give these numbers context, the graph below uses a typical home value to show how it could appreciate over the next few years using those HPES projections (see graph below). This is what you could start to earn in equity if you buy a home in early 2025.

But what does that really mean for you? To give these numbers context, the graph below uses a typical home value to show how it could appreciate over the next few years using those HPES projections (see graph below). This is what you could start to earn in equity if you buy a home in early 2025.

In this example, let’s say you go ahead and buy a $400,000 home this January. Based on the expert forecasts from the HPES, you could gain more than $83,000 in household wealth over the next five years. That’s not a small number. If you keep on renting, you’re losing out on this equity gain.

In this example, let’s say you go ahead and buy a $400,000 home this January. Based on the expert forecasts from the HPES, you could gain more than $83,000 in household wealth over the next five years. That’s not a small number. If you keep on renting, you’re losing out on this equity gain.

And while today’s market has its fair share of challenges, this is why buying is going to be worth it in the long run. If you want to buy a home, don’t give up. There are creative ways we can make your purchase possible. From looking at more affordable areas, to considering condos or townhomes, or even checking out down payment assistance programs, there are options to help you make it happen.

So sure, you could wait. But if you’re just waiting it out to perfectly time the market, this is what you’re missing out on. And that decision is up to you.

If you’re torn between buying now or waiting, don’t forget that it’s time in the market, not timing the market that truly matters. Let’s connect if you want to talk about what you need to do to get the process started today.

Is a Fixer Upper Right for You?

Looking to buy a home but feeling like almost everything is out of reach? Here’s the thing. There’s still a way to become a homeowner, even when affordability seems like a huge roadblock – and it might be with a fixer upper. Let’s dive into why buying a fixer upper could be your ticket to homeownership and how you can make it work.

What Is a Fixer Upper?

A fixer upper is a home that’s in livable condition but needs some work. The amount of work varies by home – some may need cosmetic updates like wallpaper removal and new flooring, while others might require more extensive repairs like replacing a roof or updating plumbing.

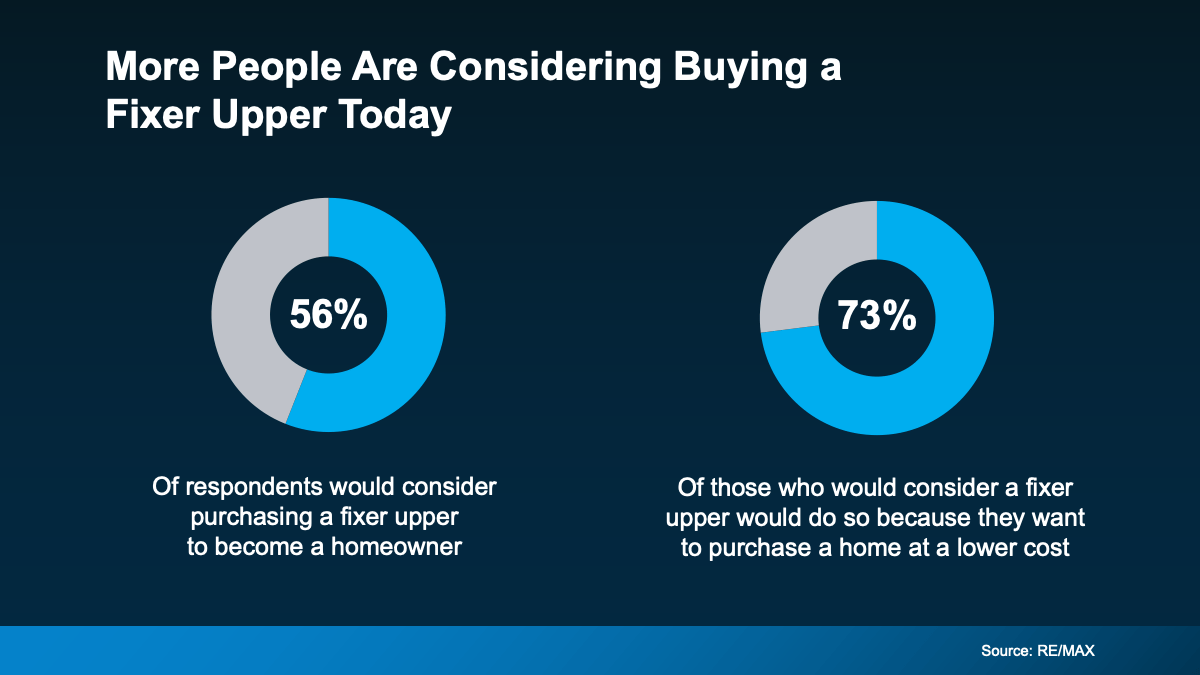

Because they need some elbow grease, these homes typically have a lower price point, based on local market value. In fact, a survey from StorageCafe explains that fixer uppers generally cost about 29% less than move-in-ready homes.

And that’s why, according to a recent survey, more buyers are considering homes that need a little extra work right now (see below):

If you’re looking for an option to get your foot in the door, and you’re willing to roll up your sleeves and do a bit of work, a house with untapped potential may be a good option.

If you’re looking for an option to get your foot in the door, and you’re willing to roll up your sleeves and do a bit of work, a house with untapped potential may be a good option.

Tips for Buying a Home That Needs Some Work

Before you buy a home that may need a makeover, here are a few things to keep in mind:

- Choose a Good Location: You can repair a house, but you can’t change where it is. Make sure the home is in a neighborhood you like or one with increasing property values and a growing number of local amenities. This way, even after you spend money fixing it up, the house will be worth more later.

- Budget for Surprises: Fixing up a house can take more time and money than you might think. Make sure you save room in your budget for unexpected repairs or other unknowns that might come up while you’re working on the house.

- Get a Home Inspection: Before you buy, hire an inspector to check out the house. They’ll help you determine the necessary repairs, so you don’t end up with expensive surprises later.

- Plan Your Priorities: When deciding what to tackle first, it helps to categorize your goals. Think of your home in three ways: the must-haves (essential repairs), the nice-to-haves (upgrades that would make life easier), and the dream-state features (luxuries you can add later). This will help you prioritize and stick to your budget.

Remember, the perfect home is the one you perfect after buying it. By starting with a fixer upper, you have the opportunity to customize a home to your liking while saving money on the initial purchase price. With careful planning, budgeting, and a little bit of vision, you can turn a house that needs some love into your perfect home.

Real estate agents are great at finding homes with potential. They know the local market and can guide you to homes where smart upgrades can add value. With their help, you’re more likely to find a house that fits your total budget and has room for worthwhile improvements.

In today’s market, where the cost of homeownership can be intimidating, finding a move-in-ready home that fits your budget can feel like a real challenge. But if you’re open to putting in a little work, you can transform a fixer upper into your ideal home over time. Let’s explore what’s possible and find a place that’ll work for you.

Don’t Let Fear or Uncertainty Hold You Back From Achieving Your Goals

How Real Estate Agents Take the Fear Out of Moving

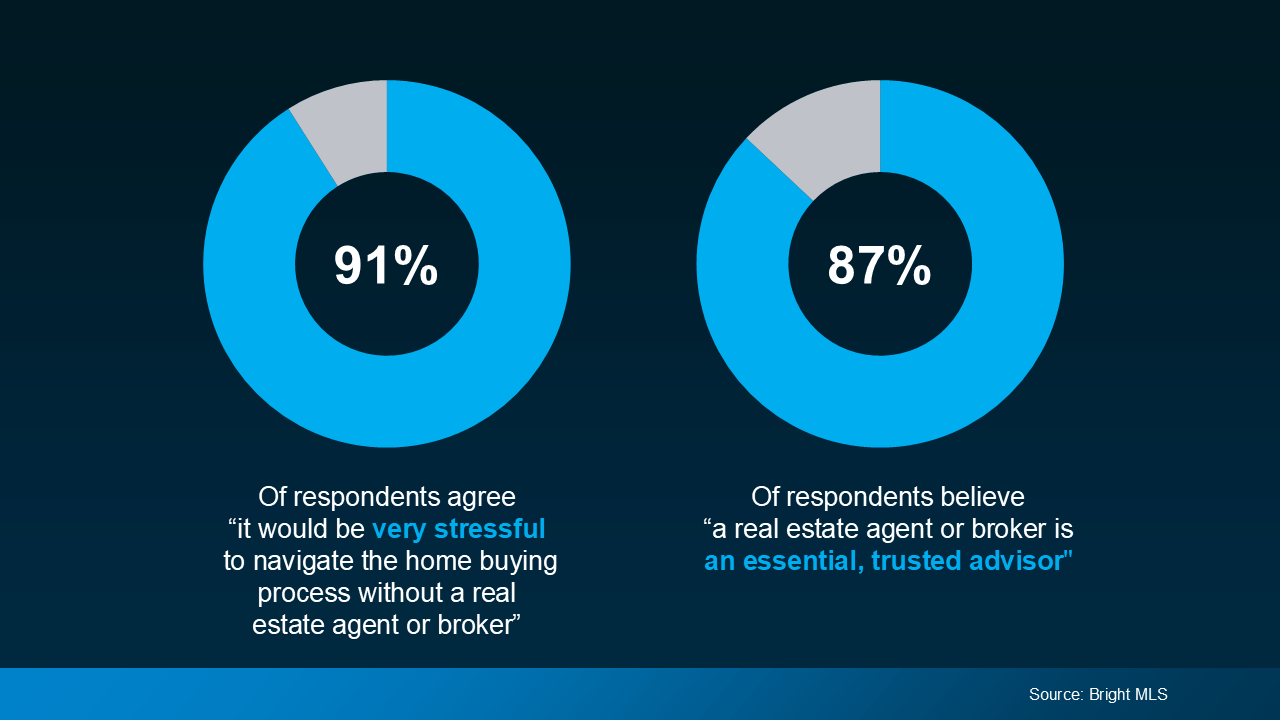

Feeling a bit unsure, or even afraid, to move with everything going on right now? The decision to move shouldn’t be scary, it should be exciting. And the best way to eliminate any fear is to work with a pro.

As Real estate agent professionals we are so much more than just transaction facilitators; we’re trusted guides to help you navigate the complexities of the housing market with confidence and ease. And a great agent can turn what may feel like a daunting process into a manageable—and even enjoyable—experience.

That’s why, in a Bright MLS survey, respondents agreed partnering with an agent is essential and helps cut down on their stress:

Here are just a few examples of why our expertise can give you so much peace of mind.

1. Explaining the Current Market

You may be seeing misleading headlines about a potential market crash, falling prices, and more. And when you’re not an expert yourself, it’s easy to get swept up in the clickbait and let that scare you. As Jason Lewris, Co-Founder and Chief Data Officer at Parcl, says:

“In the absence of trustworthy, up-to-date information, real estate decisions are increasingly being driven by fear, uncertainty, and doubt.”

As a real estate agent professionals, we’re there to help you separate fact from fiction and to debunk any headline that does more to terrify than clarify. With a deep understanding of local market trends, home values, inventory levels, and more, we can help you feel more confident in your decision.

2. Walking You Through the Process Step-by-Step

Is this your first time going through the process as a buyer or a seller? Don’t worry. Should you choose to work with me, I will walk you through every step along the way, from the initial conversation all the way to closing day. As NerdWallet explains:

“If it’s your first time buying — or selling — you’re likely to come across terms you don’t recognize and tasks that seem baffling. What’s the difference between pending and contingent? Why do you need title insurance? How thoroughly do you need to fill out disclosure forms? Your agent should be able to confidently and competently explain it all.”

And if you’ve done this before, but it’s been a while, I will tailor it to your needs. I won’t bog you down with details, but rather give you as much of a refresher as you want and need.

3. Advocating for Your Best Interests

Does the thought of dealing with the back and forth of the transaction make your palms sweaty? Put that anxiety aside. As a real agent professional, I am skilled negotiator trained for these exact scenarios. And the best part is, I work for you. So, it’s your goals I will be negotiating to fight for.

I’ll work to secure the best possible terms for you, whether it’s getting a better price as a homebuyer or negotiating a higher sale price as a seller. This removes the fear of a bad deal or being taken advantage of during the process.

4. Solving Any Unexpected Problems Quickly

Worried something is going come up that you don’t know how to handle? Rest assured, I’ve agent has you covered.

As a skilled problem-solver, I’ll not only address issues, but get ahead of them before they become deal-breakers – and that helps keep the process on track. So, if any challenges do pop up, know I have the skills and experience necessary to find a solution that works for you.

Let’s connect so you can move forward with confidence.

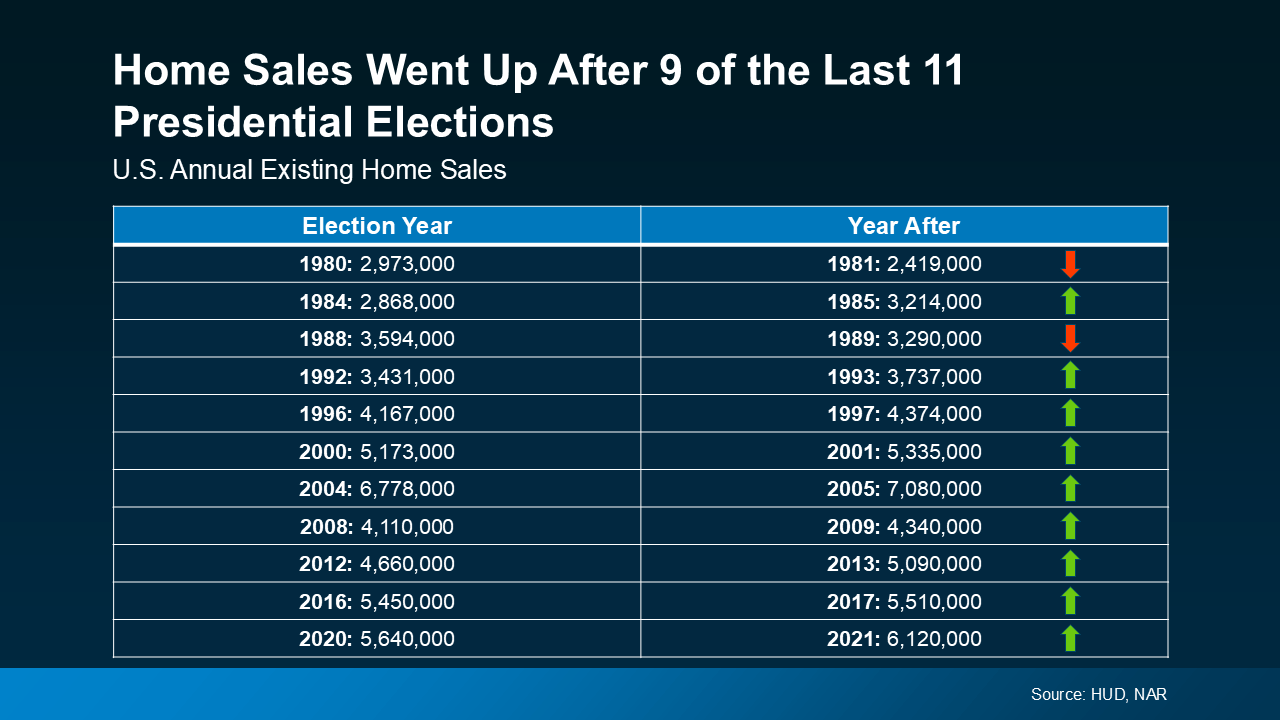

Real Estate in an Election Year

With the 2024 Presidential election fast approaching, you might be wondering what impact, if any, it’s having on the housing market. Let’s break it down.

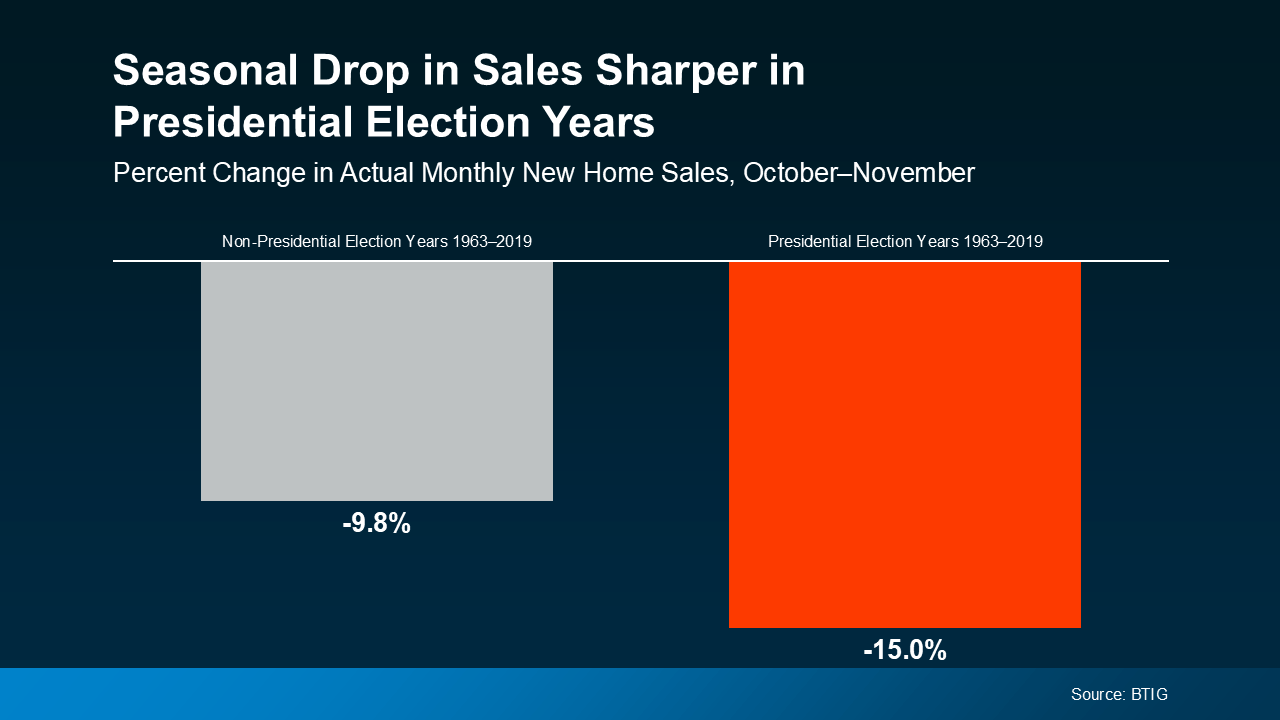

Election Years Bring a Temporary Slowdown

In any given year, home sales slow down slightly in the fall. It’s a typical, seasonal trend. However, according to data from BTIG, in election years there’s usually a slightly larger dip in home sales in the month leading up to Election Day.

Home Sales Bounce Back After the Election

The good news is these delayed sales aren’t lost forever—they’re just postponed. History shows sales tend to rebound after the election is over. In fact, home sales have actually increased 82% of the time in the year after the election.

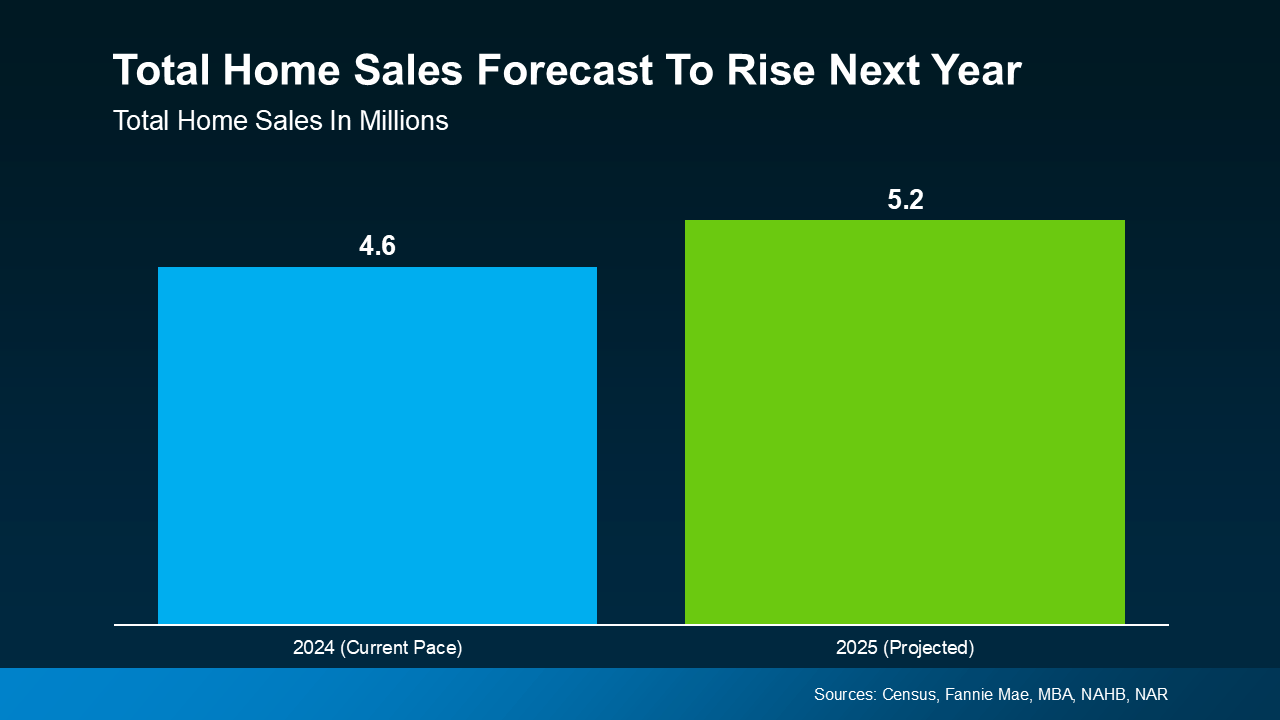

What To Expect in 2025

If history is any indicator, that means more homes will sell next year. And based on the latest forecasts, that’s exactly what you should expect. The housing market is on pace to sell a total of 4.6 million homes this year, and projections are for 5.2 million total sales next year. And that aligns with the typical pattern of post-election rebounds.

It’s important to remember that while election years often bring a short-term slowdown in the housing market, the pause is usually temporary. Those sales are not lost. Data shows home sales typically increase the year after a Presidential election, and current forecasts indicate 2025 will be no different. If you’re waiting for a clearer picture before making a move, just know that the market is expected to pick up speed in the months ahead.

Ready to Shine! New Listing Alert!

This home is sparkling and ready to shine.

Home maintenance and yard prep ✔️

Home professionally cleaned ✔️

Carpets professionally cleaned ✔️

Home staging complete ✔️

Photography & videography complete ✔️

Contractor box removed and keybox placed ✔️

Marketing flyers placed in home ✔️

Open house flyers delivered ✔️

Sign up ✔️

We’ve put in all the prep work, and now it’s time to share!

Planning To Sell Your House in 2025? Start Prepping Now…

If your goal is to sell your house in 2025, now’s the time to start prepping. Even though it might seem like there’s plenty of time between now and the new year, you should get a head start on any updates or repairs you want to make now. As Danielle Hale, Chief Economist at Realtor.com, says:

“ . . . now is the time to start thinking about what you need for your next home and then taking those steps to prepare to list . . . We have survey data that says 47 percent of sellers are taking longer than a month to get their home ready to sell, so getting them to start that process early can mean more flexibility.”

By starting your prep work early, you’ll give yourself plenty of time to get your house market-ready by the end of the year. But be sure to partner with your trusted local agent (me!) before you get started, so you have expert insight into what repairs are worth it based on your local market.

Why Starting Early Is Key

To get the best price and sell quickly, it’s important that your home looks its best. And that means it’s up to you to make the necessary repairs, declutter, and even consider updates that could add value as part of getting your house ready to list.

By starting now, you can tackle things one task at a time. Whether it’s fixing that leaky faucet, refreshing your landscaping, or painting a room, getting an early start gives you the flexibility to do the job right and with as little stress as possible. Because, if you wait to knock items off your list later on, they could quickly stack up and get overwhelming. As Realtor.com explains:

“There are some important repairs to make before selling a house, so don’t be in too much of a hurry to get your home listed … if you move too fast, buyers see right through the fact that you skipped important home renovations. And this . . . might end up costing you time and money.”

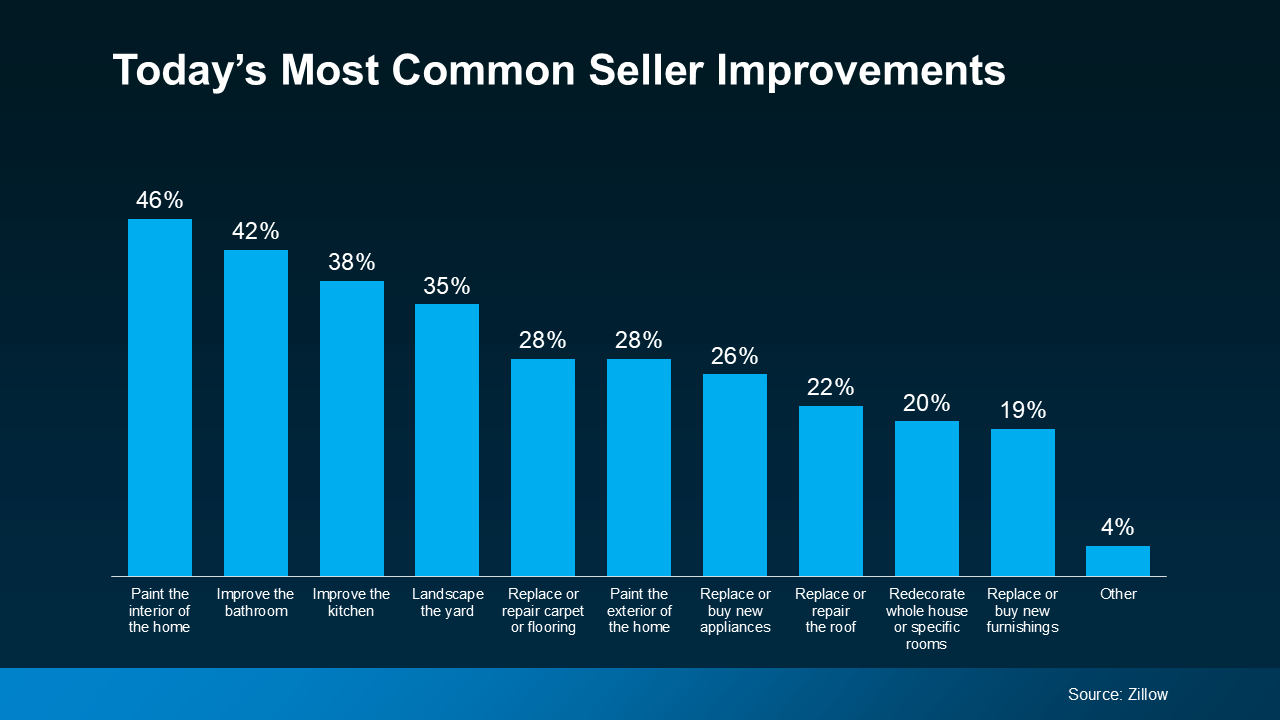

What Should You Focus On?

Feeling motivated to start chipping away at that to-do list, but not sure where to start? Here’s a look at the most common improvements other sellers are making today (see graph below):

And while that data gives you a starting point, it shouldn’t be seen as a comprehensive list. I help my clients focus on where to spending money on areas that will likely yield them a higher return based on our local data vs. focusing on those items that won’t offer as much return. This type of expert eye has been critical in helping my clients sell their home faster and for top dollar.

Thinking of selling your house next year? Don’t wait until the last minute to get it ready. By getting a head start now, you can ensure everything is in place by the time the new year rolls around.

Need advice on what to tackle first? Let’s connect.

Declutter or Keep?

When faced with a move, people often begin to re-evaluate their belongings. Should you declutter before you go? Perhaps this fresh start in a new home deserves a fresh start with new belongings too. Maybe the hassle of moving across the country with truckloads of items just doesn’t seem appealing or cost effective. It is likely your current belongings won’t fit in your new space anyways. Plus, if you are selling, a staged home tends to sell for more than it’s un-staged counterpart. Yes, you should declutter before you go.

If you have found yourself here, it is time to start decluttering and deciding which items you can part with and which you can’t live without. But how do you get rid of it all? Follow along below for key insights into making a successful yard sell and offer some of my favorite places to donate in Skagit and Snohomish Counties.

Host a Yard Sale

Hosting a yard sale is an excellent way to give a second life to your unwanted items, lighten your moving load, make room for new possessions, and potentially generate a little extra cash for the move. Here are some tips to ensure your yard sale is a success.

Separate Sell Items from Keep Items

Apart from keepsakes and heirlooms, a good rule of thumb is if you haven’t used something in over a year it is probably something you can live without and can contribute to the get rid of pile. Another approach is if an item no longer brings you joy or an inkling of excitement then it is likely past its life with you but could bring joy to someone else. Add it to the get rid of pile! Be sure to separate the items you are parting with from the items you are keeping. If you wish to be extra organize sort piles by price ranges. Try color coding your items with stickers to demonstrate your selling price.

Price Flexibility

Keep in mind that people like to negotiate the price. Determine now what items you are willing to negotiate on and which items you don’t feel there is room to budge. Price accordingly. Remember yard sales are not meant to get rich from, but instead helping to reduce your moving load and offer extended life to your unneeded items to keep them out of the waste plants.

Generate Neighborhood Excitement

Plan your yard sale in advance. It is likely you have friends and neighbors that have stuff they would like to part with too. Make it a neighborhood event so that multiple yard sales happen on the same day and same time. Together you can pitch in for signage that can be posted around town directing traffic to your neighborhood yard sale. This will attract more buyers and reduce your overhead costs. At the end of the sale, celebrate your success with a neighborhood gathering like a BBQ dinner or potluck.

Promote Your Neighborhood Yard Sale on Social Media

Boost the visibility of your yard sale by leveraging social media and neighborhood apps. Start by creating a Facebook event page and inviting all your friends. Share the event on Twitter with a fun hashtag and offer a prize for those who repost about your sale. Post a carousel of the items for sale on Instagram to attract more attention. Additionally, use Nextdoor or another neighborhood app to reach people beyond your immediate area. No matter what knick-knacks you uncover, expanding your audience will help ensure they find the right home. You might also wish to list your items on Facebook Marketplace or your local Buy Nothing groups. Check in your local area for local consignment shops that will sell your items for you and you receive a portion of the sale price in return.

Payment Options

Keep in mind that most people don’t carry cash anymore. It pays to have a variety of payment options so that negotiators can’t finagle your price due to lack of cash on hand. Try offering PayPal, Venmo, Zelle, or another form of digital payment. You will likely discover more sales and turn passer-buyers into buyers.

Donate your leftovers

The final step to declutter before you go is immediately after your sale, bag up the leftovers and take them to your local donation center. Otherwise, they will find their way right back into your house, garage, or storage and you will end up paying to transport them to your new home. Here is a list of several donation centers in Skagit and Snohomish Counties.

Arlington:

Skagit Valley:

North Cascades:

Anacortes:

Housing & Economic Update: Key Numbers to Know 10/7/2024

Windermere Principal Economist Jeff Tucker takes a look at the numbers in the Oct. 4 jobs report, how it impacted mortgage rates, and his prediction for rates in the coming months. Click HERE to watch his prediction.